Barrick Gold (TSX: ABX)(NYSE: ABX) represents everything that went wrong in the gold mining industry.

The past several years have been marked by a long list of expensive mistakes. The company purchased asset after asset at ridiculously high prices that blew up when commodity prices imploded. Its attempt to diversify outside of its precious-metals business into copper mining resulted in nearly $4 billion in write-offs. And development at the company’s flagship Pascua Lama was billions of dollars overbudget before being shut down.

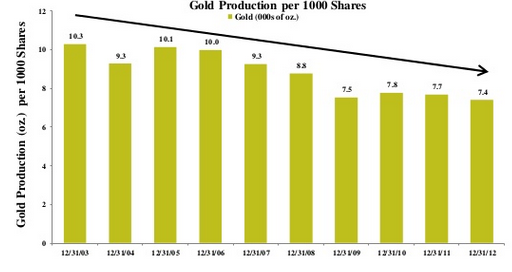

Shareholders have paid dearly for these missteps. Today, the company is saddled with over $13 billion in debt and the stock trades at a discount to peers on most valuation metrics. But if I had one chart to sum up everything that’s wrong with Barrick, it would be this one.

Source: Two Fish Asset Management

Since 2003, Barrick has spent over $40 billion on capital expenditures and acquisitions. Shareholders have actually paid an additional $4 billion into the business. And in exchange for this, gold production per share actually declined 30% between 2003 and 2012.

Sure, on many metrics — such as revenue, EBITDA, and employees — Barrick is a larger company. But through the lens of the investor, all of this expansion has done nothing to grow shareholder wealth. In essence, shareholders have sacrificed billions of dollars in potential dividends and share buybacks in order to finance management’s empire ambitions.

How did this happen? The board tied its compensation structure primarily to growth benchmarks — namely adjusted free cash flow and adjusted EBITDA — without taking into account the capital required to grow those metrics.

The board has a misguided view that growing production, cash flow, and reserves is what drives investment returns. They have placed no emphasis on any per share measures of these criteria. Building a compensation scheme around EBITDA and free cash flow measures without accounting for shares outstanding or capital employed is flawed.

How can this be fixed? Fortunately the company is starting to address this issue. At Barrick’s annual general meeting later this month, the board plans to announce a new executive compensation plan in order to better align the interests of management with shareholders.

What metrics should be used to grade management? Once again, everything must be considered from the perspective of shareholders. The board should not use operating cash flow, but operating cash flow per share. The board should not use not gold production, but gold production per share. The board should not use not reserve replacement, but reserve replacement per share.

In addition, management should also be forced to hold more stock. According to Barrick’s 2013 proxy circular, the company’s board of directors owns only 0.3% of outstanding shares combined. No wonder management presided over this massive destruction of shareholder value; it wasn’t their money on the line. By forcing management to hold a larger stake in the company, they’re incentivized to think like business owners rather than high-paid managers.

Foolish bottom line

Does management play alongside shareholders? Is their motivation to win big if the company succeeds? Or is it their own paycheck? Barrick shareholders have learned a valuable lesson: Make sure the incentives of management of investors or pay the price.