Shares of Tilray Brands (TSX:TLRY) have witnessed a selloff after announcing its latest quarterly financial results on October 4. Since then, the TSX-listed TLRY stock has lost nearly 9% of its value to currently trade at $2.81 per share, bringing its market cap to $2 billion and extending its year-to-date losses to 23.4%.

Before we discuss whether or not Tilray stock looks attractive to buy on the dip today, let’s take a closer look at some key highlights from its recently released quarterly earnings report.

Image source: Getty Images

Tilray’s first-quarter results

If you don’t know much about it already, Tilray is a New York-headquartered company that primarily focuses on selling cannabis-based consumer packaged goods and beverage alcohol to consumers. Out of its total four business segments, the company generated most of its revenue from its distribution and cannabis segments in its fiscal year 2023 (ended in May). Geographically, North America was its biggest market segment that fiscal year.

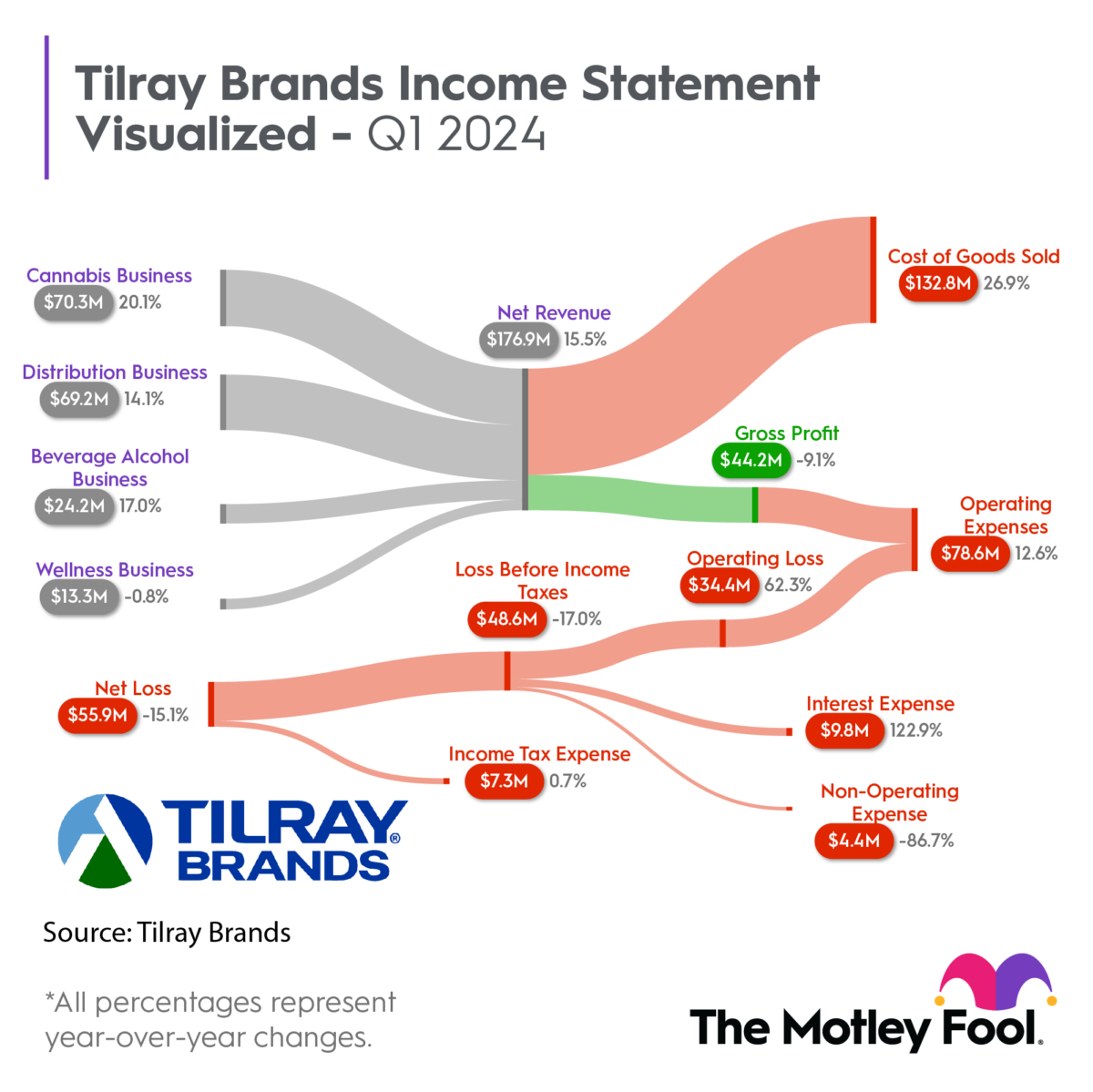

In the first quarter of its fiscal year 2024 (ended in August), Tilray’s total revenue increased by 15.5% YoY (year over year) to US$176.9 million, exceeding Street analysts’ estimate of US$173.6 million. With this, the cannabis giant’s adjusted quarterly net loss narrowed to US$55.9 million in the August 2023 quarter from US$65.8 million in the August 2022 quarter. However, its bottom line missed analysts’ estimates, who were expecting it to report a quarterly net loss of US$34.2 million. This could be one of the reasons why TLRY’s share prices slid after its earnings event, also pressuring other cannabis stocks.

These segments led its financial growth

The positive growth in the cannabis giant’s first-quarter top line could be attributed to strong sales growth numbers from its cannabis, beverage alcohol, and distribution segments. TLRY’s cannabis sales grew positively by 20.1% YoY last quarter to US$70.3 million despite facing currency headwinds, and beverage alcohol revenue grew positively by 17% from a year ago to US$24.2 million.

Similarly, its distribution sales went up by more than 14% YoY in the August quarter to US$69.2 million, as you can see in the chart above. While Tilray’s wellness segment quarterly revenue remained flat YoY on a constant-currency basis, it declined slightly to US$13.3 million due to currency headwinds.

Despite positive contributions from all business segments except cannabis, Tilray’s overall adjusted gross margin shrank to 28% last quarter from 32% a year ago. It’s important to note that the company’s cannabis segment gross margin in the August 2022 quarter benefited from the HEXO advisory fee revenue, and this advisory revenue didn’t duplicate after Tilray completed the HEXO acquisition in June 2023.

Is Tilray stock a buy today?

Despite the ongoing macroeconomic challenges, Tilray’s cannabis market share strengthened in Canada in the first quarter to 13.4%. Moreover, its overall business remains financially healthy, with continued positive growth in its revenue and profitability. For example, the company’s distribution segment profitability improved due mainly to a favourable sales mix and lower production costs.

Also, higher beer sales and its recent acquisition of Montauk Brewing Company helped it expand the beverage alcohol segment’s gross margin in the latest quarter. You can expect the segment’s profitability to keep improving in the coming quarters as Tilray recently strengthened its position in the U.S. craft beer market further by completing its acquisition of eight beer and beverage brands from Anheuser-Busch earlier this month.

Given these positive fundamental factors and expectations of stronger profits, TLRY could be a really attractive TSX stock to buy on the dip today, especially if you can hold it for the long term.