If you’re 45 years old and feel behind on retirement savings, you’re not alone. Life happens. Maybe you were raising kids, paying down a mortgage, supporting a sick family member, or simply didn’t understand the importance of investing earlier on.

Now, age 60 is only 15 years away, and the thought of relying solely on Canada Pension Plan (CPP) and Old Age Security (OAS) for retirement income doesn’t feel very comfortable.

It’s true that younger investors have a huge advantage. They have time to compound and recover from bear markets. But being 45 doesn’t mean you’re out of options. It just means the margin for error is smaller and the discipline required is higher.

If you want a realistic shot at catching up, the formula is simple: max out your Tax-Free Savings Account (TFSA) every year and invest it in a low-cost S&P 500 index exchange-traded fund (ETF). It’s aggressive. It requires a high risk tolerance. But it can work.

Source: Getty Images

Start With Your TFSA

For 2026, the TFSA contribution limit is $7,000. That may not sound like much, but over 15 years, that’s $105,000 in new contributions alone (assuming they don’t keep hiking the annual limit).

The TFSA is powerful because all investment growth within it is tax-free, whether from dividends, interest income, or capital gains. Moreover, withdrawals can happen anytime and are not subject to tax.

Unlike a Registered Retirement Savings Plan (RRSP), you don’t get a tax deduction upfront. But the flexibility and tax-free compounding make the TFSA incredibly valuable, especially if your income in retirement may not be dramatically lower than it is today.

If you can, lump sum the $7,000 at the beginning of each year. Historically, investing earlier has produced better results than waiting. If that makes you nervous, you can dollar-cost average by splitting the $7,000 into monthly or weekly contributions.

Why the S&P 500?

With only 15 years to work with, you likely need meaningful equity exposure. The S&P 500 represents 500 large, established U.S. companies that generate profits, reinvest in growth, buy back shares, and pay dividends. Over time, those forces compound. You’re buying the market and letting capitalism do the work.

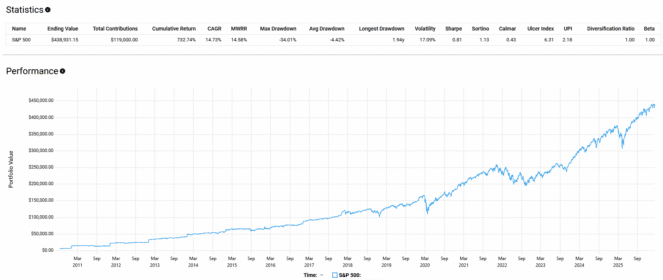

Consider the period from September 2010 to February 2026. An investor who started with $7,000, added $7,000 every year, reinvested all dividends, kept fees low, and held everything inside a TFSA would have contributed $119,000 in total. The ending value of that portfolio would have grown to $438,931.15. That represents a 14.73% annualized return and a cumulative gain of 722.7%.

But it was not a smooth ride. In an average year, the portfolio swung roughly 17% up or down. During the March 2020 COVID crash and the grinding 2022 bear market, the maximum drawdown reached 34.01%. If you pursue this strategy, you must accept that sharp temporary losses are part of the process. The biggest risk is not volatility itself. It’s abandoning the plan at the worst possible moment.

To keep more of the return working for you, fees must stay low. One simple Canadian-listed option is BMO S&P 500 Index ETF (TSX:ZSP), which charges a 0.09% expense ratio. That means just $9 per year for every $10,000 invested.

This approach is not guaranteed to make you whole. Markets don’t promise anything. But consistent TFSA contributions, broad diversification through the S&P 500, reinvested dividends, and the discipline to stay invested give you a fighting chance.