Magna International (TSX:MG) stock has been under pressure since the Aurora-based automotive industry giant released its fourth-quarter 2025 earnings in February. Down 17.5% over the past month, many investors could be wondering if the wheels are coming off MG stock. This correction period could actually be a lucrative entry point for long-term oriented investors with a 10-year or longer investment time horizon. Let’s explore why the deeply undervalued Magna stock is worth your attention right now.

Source: Getty Images

Magna stock’s earnings paradox: A beat with a warning

Magna stock’s decline initially seems counterintuitive when looking at the February 13, 2026, earnings release. The company actually delivered a “beat and raise” on key metrics. Fourth-quarter sales reached US$10.8 billion, surpassing a market consensus estimate of US$10.5 billion. Adjusted diluted earnings per share (EPS) of US$2.18 also handily beat Bay Street analysts’ US$1.81 expectation.

Trouble started with management’s near-term forecasts. While Magna’s 2026 guidance for adjusted EPS has been set at a healthy range of US$6.25 to US$7.25 (higher than the US$5.99 Bay Street estimate), management significantly lowered its 2026 sales guidance from an earlier range around US$48.8 billion to US$41.9–US$43.5 billion. This downward revision reflects a more cautious outlook on global vehicle production volumes and program roll-offs in Magna’s Complete Vehicles segment.

A current geopolitical weight: The 2026 Iran war

Selling pressure on Magna stock has intensified following the outbreak of the 2026 Iran war. The conflict has led to an immediate surge in global oil prices, with WTI crude soaring to US$100 per barrel as the Strait of Hormuz – an oil trade route responsible for a fifth of global oil supply – remains effectively blocked.

For a global car manufacturer like Magna, this geopolitical shock is a triple threat. First, it spikes logistical and input costs. Second, it threatens to reignite significant global inflation, potentially forcing central banks to keep raising interest rates higher for longer. Third, anxiety and higher interest rates may dampen consumer sentiment for large discretionary purchases like automobiles.

The current 17.5% one month drop in MG stock is a reflection of the market pricing in a potential moderate recession scenario in which global economic growth slows under the weight of an energy shock.

Why Magna stock may recover to enrich long-term investors

Despite current headwinds, the valuation logic for holding Magna stock long term is compelling. Magna stock trades at a significant discount to historical valuation multiples, it’s a dividend stock that keeps raising its payouts, and management is adding a stock repurchase yield into the total returns mix.

Magna stock trades at a single-digit forward price-earnings (P/E) multiple of 8.1 times the midpoint of its 2026 earnings guidance (US$6.75). This is significantly below its -year historical average P/E above 13. Even if earnings come in at the low end of guidance, the stock remains historically cheap. Shares may recover as the global outlook for the automotive industry improves. It will.

Further, MG stock is a dividend growth fortress. Management celebrated a 16th consecutive year of dividend raises in 2025. With a yield currently at 3.5%, investors will be compensated with quarterly cash drops as they await a cyclical recovery.

Most noteworthy, Magna is aggressively repurchasing its stock. The company intends to repurchase the remaining 22 million shares authorized under its current Normal Course Issuer Bid (NCIB), which is set to expire on November 6, 2026, providing significant support for the share price during this volatility.

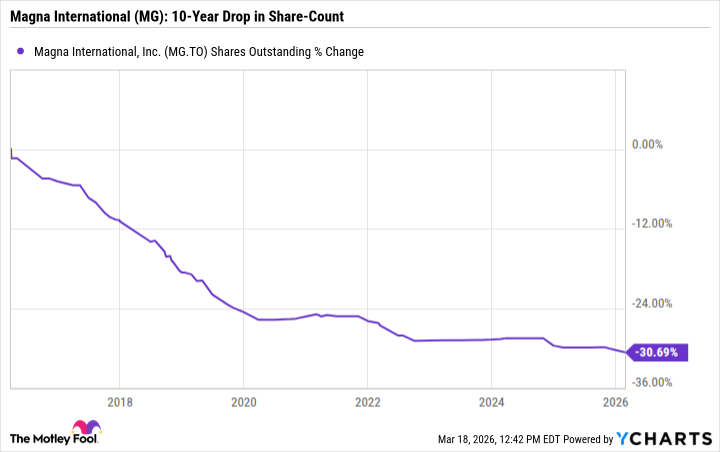

MG Shares Outstanding data by YCharts

Magna has reduced its share count through repurchases by more than 30% during the past decade.

MG stock’s long-term outlook

To justify a long-term hold on Magna stock, one must look beyond the internal combustion engine. Over the next decade, Magna’s recovery will lean on its investments in the software-defined smart vehicle platforms. The global automotive software market may grow at rates up to 11.2%, annually. Magna is already a top-five player in this space, leveraging its expertise in Advanced Driver-Assistance Systems (ADAS) and electric powertrains to capture more value per vehicle.

Furthermore, Magna’s “Operational Excellence” program may add 200 basis points to margins in the near term, creating a leaner, more profitable and more valuable enterprise, even in a low-growth environment.