What if you could collect a near-8% yield every single month, defer taxes almost entirely, and own a slice of one of the largest manufactured home community portfolios in Canada – all at a discount? That’s the investment opportunity unfolding at Firm Capital Property Trust (TSX:FCD.UN). The diversified real estate investment trust’s (REIT) just posted first-quarter 2026 results signal a real and sustained turnaround in the high-yield monthly dividend stock as a flurry of acquisitions promise to rewrite its future.

Source: Getty Images

Firm Capital Property Trust’s: AFFO surges, payout ratio tightens

Firm Capital Property Trust’s latest quarterly operating results show net operating income up 5% year over year, while adjusted funds from operations (AFFO) per unit jumped 10% to $0.129. The most appealing headline for income investors: FCD.UN’s AFFO payout ratio fell from a dangerous 111% a year ago to 101% in the first quarter of 2026. That’s not yet sustainably within management’s 85%–95% AFFO payout rate target, but the direction is undeniable. Distributions are getting sustainably safer.

Most noteworthy, the REIT’s portfolio is changing shape. Grocery-anchored retail now contributes 49% of net operating income (NOI), down from 54% six months ago. Industrial properties’ contribution to NOI sits at 29%, while manufactured home communities (MHC) have swelled from 18% to 22% of NOI. That MHC slice is about to get much bigger in 2026.

FCD.UN becoming Canada’s MHC king, in partnership with insiders

In May, FCD.UN bought a 50% stake in a 103-site MHC in Alberta. Far more significant is a pending $218 million deal for 10 MHC properties with 1,649 sites across Alberta and Saskatchewan. Expected to close this quarter, the acquisition will make Firm Capital one of the largest single owners of MHC properties in Canada. Both transactions are within Firm Capital’s joint venture with SunPark, an entity tightly linked to management. The joint acquisitions continue a plausible pattern of high insider co-investment. When the people running the trust write big cheques alongside you, incentives usually line up.

Once these new portfolios are fully integrated, the NOI contribution from MHC will leap, bringing more stable, recession-resistant income. Manufactured home communities see sticky occupancy, low turnover, and steady rent growth, offering a buffer when retail or industrial property economics wobble.

Invest for distributions that offer unique tax-management advantages

FCD.UN’s monthly distribution of $0.0433 per unit remains heavily tax-advantaged. Management estimates 95% of the 2026 payout will classify as return of capital (ROC). In a non-registered account, that means you’ll defer tax until your adjusted cost base hits zero – potentially affording you years of tax-deferred monthly income. It’s a rarity among Canadian REITs, which typically dish out fully taxable income (unless you stash them in a TFSA). That said, ROC components remain variable year-to-year, and you may still wish to use the TFSA’s tax shelter to avoid cost-basis-tracking hustles.

At the REIT’s current unit price around $6.60, new investors earn a 7.9% yield. Given the REIT’s most recent net asset value (NAV) per unit of $7.98, new investors can buy high-yield monthly dividend-paying assets at a 17% discount to their fair value.

Is the distribution truly safe yet?

Payout ratios are improving, and the current 101% is much better but not bulletproof. Yet with two accretive MHC deals layering on cash flow, the trend points toward a sustainable sub-100% payout ratio in the near future.

Interestingly, portfolio occupancy levels remain high and healthy across the portfolio, and rising NOI provides a distribution cushion.

Management has already declared monthly distributions payable through October 2026. Cash flow visibility on this monthly dividend stock is very high, and management confidence in the sustained payout remains high.

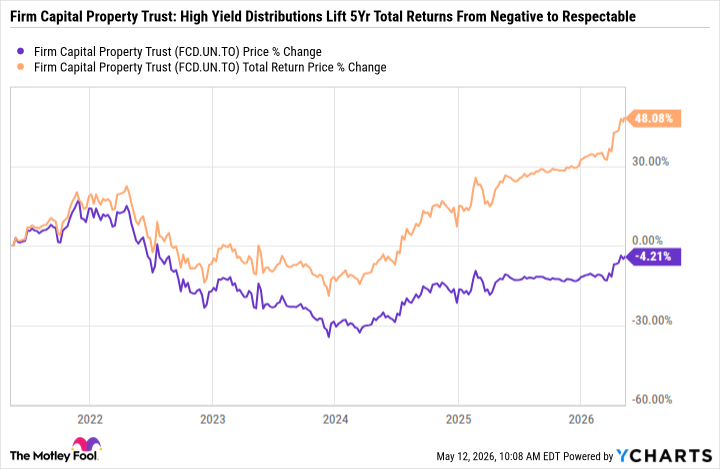

Firm Capital Property Trust’s high-yield monthly distribution has single-handedly lifted total returns on the REIT during the past five years. Capital gains have been catching up lately.

Investor takeaway

Firm Capital Property Trust is morphing into a Canadian MHC powerhouse with a monthly, near-tax-free distribution. First-quarter results showed plausible momentum in AFFO growth, with payout coverage improving and big portfolio-expanding deals nearly sealed.

The REIT’s 7.9% yield, insider alignment, and a 17% discount to NAV offer a compelling monthly-dividend investment package. If distribution sustainability can finally crack that 100% ceiling for good, today’s buyers may look very smart long term.