It’s RRSP season! If you haven’t yet maxed out your 2021 contribution limit, you have until March 1, 2022. TFSA limits have also increased, giving you an additional $6,000 in contribution room for 2022.

If you’ve already maxed these out and invested, give yourself a pat on the back! But for some of you, I’m guessing you’re now wondering what to do with the excess cash.

My suggestion is to invest it in a taxable account. You can hold the same investments as in your RRSP and TFSA. The difference is you pay taxes on the dividends and capital gains (which are taxed at a favourable rate relative to your income).

However, a cool exchange-traded fund (ETF) from Horizons ETFs allows you to eliminate dividend tax and delay capital gains tax, potentially saving significant amounts. Let’s take a look at how they work!

Total return swaps, and how they work

Traditional ETFs hold a basket of underlying stocks and sell you shares of that basket. These ETF shares trade on an exchange and their prices fluctuate based on the underlying holdings.

Horizons ETFs, and in particular, Horizons S&P/TSX 60 Index ETF (TSX:HXT) are quite different. HXT does not hold the underlying 60 stocks in the index. Instead, it uses a derivative called a total return swap (TRS) to replicate the performance of the index.

Essentially, Horizons enters into a swap agreement with a counterparty. When you buy units of HXT, your investment is held in cash as collateral. The counterparty is then obligated to remit to Horizons the total return of the index (capital gains + dividends).

For example, if the stocks in the index increase by 8% and pay a 2% dividend, the counterparty will pay 10% to Horizons (minus fees), and HXT will increase in price by 10% (again, minus the fee).

What are the benefits?

Firstly, the tracking error of HXT is incredibly small. Because the counterparty is obligated to deliver the total return of the index, they minimize turnover and the trading costs that come with traditional ETFs. The dividends are also perfectly reinvested, which boosts returns.

The management expense ratio (MER) is rock bottom at 0.03% due to the use of swaps. This is the cheapest you’ll find in the Canadian ETF market right now.

Finally, holding HXT in your taxable account is highly efficient. Because there are no distributions, you pay no dividend tax. Your only pay capital gains tax, which can be deferred until you are ready to sell.

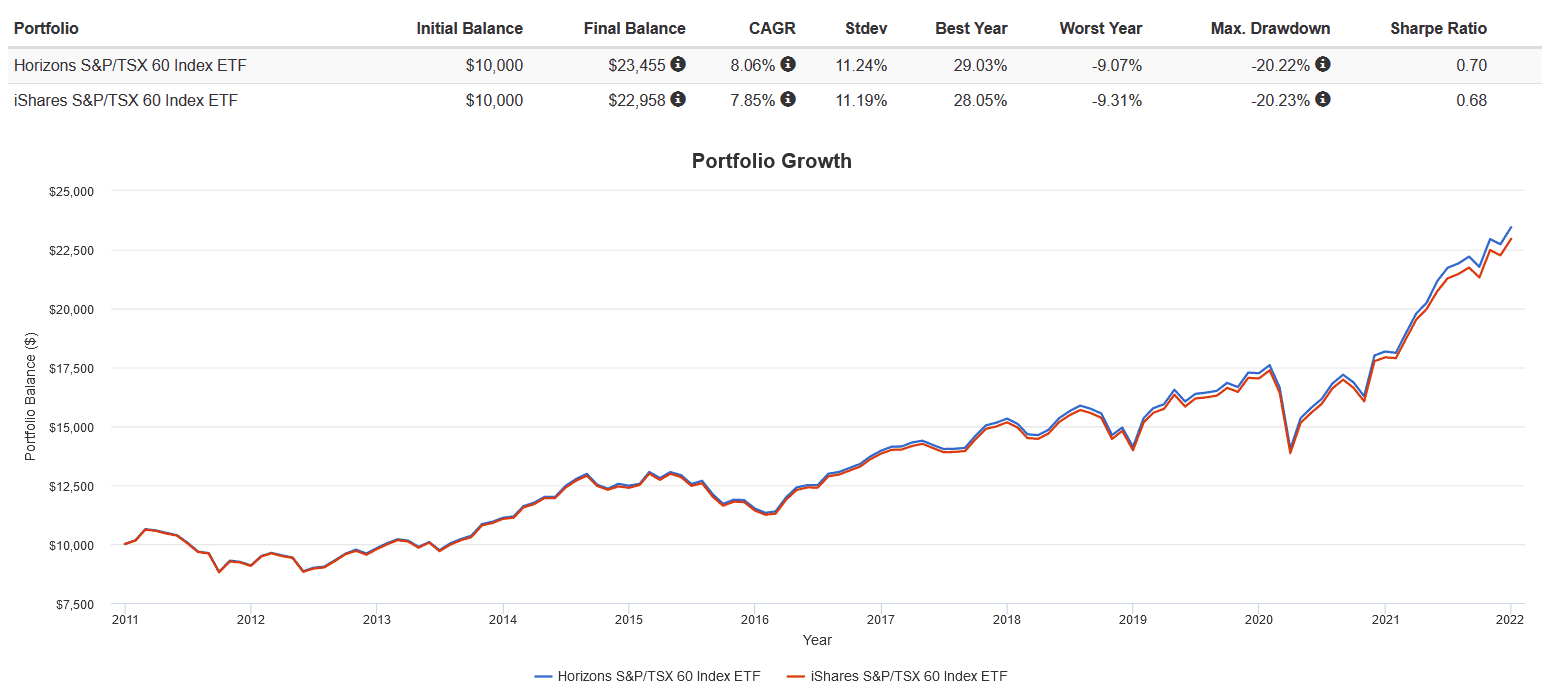

The backtest below from 2011 with all dividends reinvested shows outperformance of HXT compared other S&P TSX/60 Index ETFs due to the afformentioned advantages:

What are the risks?

Complex derivative-based products like HXT also come with a unique set of risks. While Horizons has done a great job of mitigating them, investors should still be mindful.

First up is counterparty risk, the possibility that the counterparty will fail to pay a return equal to that of the index when owing. I’m not worried about this. The main counterparty is the National Bank of Canada. It would be highly unlikely for a Big 6 bank to default on this obligation.

Moreover, in the event that does happen, the underlying index would likely tank and eliminate the counterparty exposure (the returns owed, which are now zero or negative as the index has gone down) anyway, and you would get the cash collateral held (losing any gains but keeping the principal).

The second risk is regulatory risk. The government might eliminate the tax loophole that turns taxable dividend income into capital gains. It if happens, HXT investors would be forced to sell and and realize all of those capital gains, which would cause a big one-time tax bill.

The Foolish takeaway

Investors using a taxable account can use HXT to eliminate dividend tax and defer capital gains tax, saving themselves money. HXT also has lower fees and less tracking error compared to traditional index ETFs of its class. As long as you’re mindful of the counterparty and regulatory risk, HXT can be an excellent addition to your holdings.