Welcome to a series where I break down and compare some of the most popular exchange-traded funds (ETFs) available to Canadian investors!

The most famous index, and the benchmark many professional investors measure themselves against, is the S&P 500. The S&P 500 tracks the largest 500 companies listed on U.S. exchanges and is widely seen as a barometre for overall U.S. stock market performance. It makes for a great passive investment.

However, beyond the well-known S&P 500 Index lies another +3,000 mid- and small-cap stocks comprising the remainder of the U.S. stock market. Vanguard provides a set of low-cost, high-liquidity ETFs that offer exposure to these stocks.

The two tickers up for consideration today are Vanguard S&P 500 Index ETF (TSX:VFV) and Vanguard U.S. Total Market Index ETF (TSX:VUN). Which one is the better option? Keep reading to find out.

VUN vs. VFV: Fees

The fee charged by an ETF is expressed as the management expense ratio (MER). This is the percentage that is deducted from the ETF’s net asset value (NAV) over time and is calculated on an annual basis. For example, an MER of 0.50% means that for every $10,000 invested, the ETF charges a fee of $50 annually.

VUN has an MER of 0.16% compared to VFV at 0.07%. Both are small, and the difference comes out to around $9 annually for a $10,000 portfolio. Still, VUN is more than twice as expensive as VFV, which can make a difference when held for the long term.

VUN vs. VFV: Holdings

VUN track the CRSP US Total Market Index. The index is comprised of more than 3,500 U.S.-listed stocks. Around 82% of the index is dominated by the large-cap stocks found in the S&P 500, with another 12% in mid-caps and 6% in small caps.

VFV tracks the S&P 500 Index, which holds 502 U.S. large-cap stocks according to their market weights. The index has almost no mid-caps and zero small-caps. As a result, its top holdings are more concentrated.

Both ETFs get their exposure by holding their U.S. ETF counterparts in a “wrapper” structure. As a result, both ETFs suffer from a 15% foreign withholding tax on the dividends, which can cause a slight drag over time but shouldn’t be a cause for concern.

In addition, when you buy a Canadian ETF like VUN or VFV that holds an U.S. ETF, the difference between the CAD-USD pair can also affect the value of the Canadian ETF beyond the share price movement of the underlying stocks.

Unhedged ETFs like VUN and VFV accept this phenomenon. What that means is if the U.S. dollar appreciates, the ETF will gain additional value. Conversely, if the Canadian dollar appreciates, the ETF will lose additional value. This introduces extra volatility that could affect your overall return.

VUN vs. VFV: Historical performance

A cautionary statement before we dive in: past performance is no guarantee of future results, which can and will vary. The portfolio returns presented below are hypothetical and backtested. The returns do not reflect trading costs, transaction fees, or taxes, which can cause drag.

Here are the trailing returns from 2014 to present:

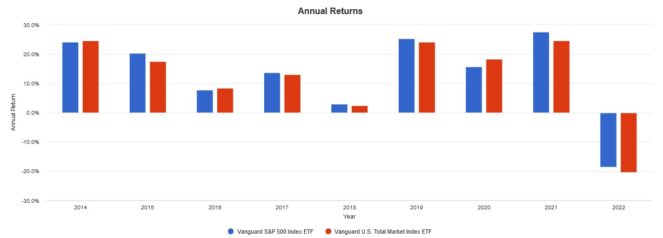

Here are the annual returns from 2014 to present:

Both ETFs have virtually identical performance, with VFV having a very slight edge. I chalk this up to the fact that the large-cap stocks in VFV have done exceptionally well in the last few years and the lower MER charged by VFV. In the future, VUN may catch up, as the higher risk from small caps can increase returns.

The Foolish takeaway

If I had to pick and choose one ETF to buy and hold, it would be VFV. The S&P 500 and the CRSP Total U.S. Market indexes are 0.99 correlated. While the small caps might make a difference in the long term, the difference between a 0.07% and 0.16% MER is worth picking VFV for me. The two can make a great tax-loss harvesting pair in a taxable account, though.