If 2025 taught Canadian dividend investors anything, it’s that high dividend yields come with low dividend safety. There’s a trade off, and a balance somewhere. But there are exceptions, too.

We watched telecom giants pause dividend growth (I’m watching you, TELUS), and a 56% dividend cut at BCE. We saw a whole dividend suspension at PetroTal in November, and a 40% dividend cut at Northland Power was necessary to sustainably finance its massive offshore wind energy development pipeline.

Basically, yields close to or above the 7% scream risk! However, extra due diligence can add confidence when selecting the best high-yield dividend stocks to buy for the long term. The most valuable asset in a dividend portfolio isn’t just current passive income — it’s future cash flow visibility.

That’s why, despite the noise in the broader market, with its 6.1% payout, Enbridge (TSX:ENB) remains the high-yield stock I’m most comfortable holding for the next decade, and at least for the next five years.

Source: Getty Images

The comfort in Enbridge stock’s capital investment backlog

The primary reason I’m comfortable with Enbridge is that its future isn’t based on guessing oil prices; it’s based on contracted “take-or-pay” pipelines cash flows and an expanded construction schedule.

Enbridge currently sits on a secured capital program of approximately $35 billion entering service through 2030. This isn’t “planned” or “aspirational” spending. The funding is allocated to projects that are commercially secured, and “utility-like” investments that will diversify its revenue, earnings and cash flow profile.

Management has confirmed roughly $8 billion of these projects will enter service in 2026.

These projects should generate reliable cash flow immediately upon completion, directly supporting the 6.1% dividend.

When you buy Enbridge stock today, you are buying the current pipeline network, a growing natural gas utility, and a renewable energy stock with a pre-funded, non-dilutive growth pipeline that extends well into the next decade.

A boring, yet beautiful passive-income growth engine

Enbridge’s medium-term financial guidance promises respectable operating earnings growth rates and stronger distributable cash flow profile. While other high-yielders are struggling to maintain their payouts, Enbridge has reaffirmed a steady growth trajectory that income investors should love.

Management targets 7-9% growth in earnings before interest, taxes, depreciation, and amortization (EBITDA) in 2026, with EBITDA and distributable cash flow (DCF) growth normalizing at 5% through 2030.

This creates a compelling mathematical floor for your total returns. If you buy the stock today at a 6.1% yield and the company grows cash flow by 5% annually, you are looking at a potential total return of about 11% per year, without requiring any valuation multiple expansion or hype.

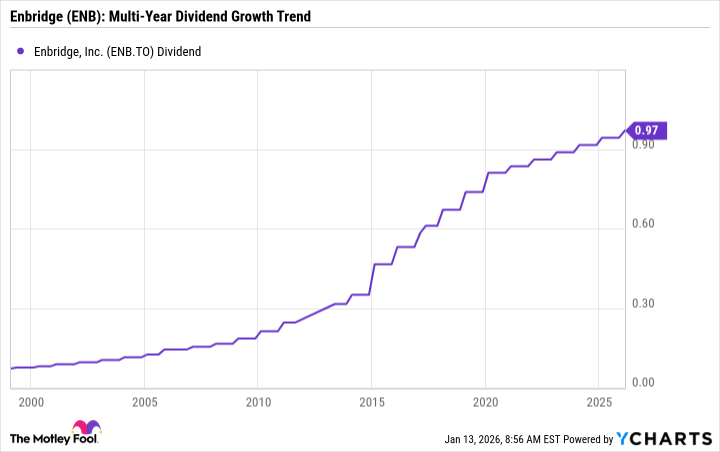

The ENB stock dividend: A 31-year growth streak

ENB Dividend data by YCharts

There’s valuable comfort in knowing that management prioritizes growing Enbridge stock’s dividend payout.

Just recently, Enbridge announced a 3% dividend increase for 2026, marking its 31st consecutive year of raises. While 3% might sound modest compared to the hikes of a decade ago, it looks sustainable. If the company manages a 5% growth rate target for DCF, and perhaps, the dividend, investors who buy ENB stock today could see yields grow to 7.5% by 2030.

Enbridge’s cash flow payout ratio remains healthy under 70%, and with the company projecting $5.70 to $6.10 in DCF per share for 2026, the dividend ($3.88 annualized) is well-covered. Management is effectively retaining enough cash to self-fund that massive $35 billion backlog we mentioned, reducing the need to issue equity or load up on dangerous amounts of debt.

The Foolish bottom line

A 6.1% yield usually comes with a catch. In Enbridge stock’s case, the “catch” is that you have to accept boring, single-digit growth rates rather than explosive tech-sector gains, and Bay Street could add execution risks on new low-carbon projects to the company’s equity risk profile.

But looking at the insiders’ recent data, the $35 billion backlog, the locked-in regulated rates, and the 5% medium-term growth target, I see a company that has already built the “dividend” bridge to 2030. For a long-term passive-income portfolio, that’s the kind of comfort I’m looking for.