Canadian investors often treat the big bank stocks as interchangeable, but as we navigate 2026, Bank of Montreal (TSX:BMO) and Bank of Nova Scotia (TSX:BNS), or Scotiabank stock, are offering distinct propositions. Both institutions command massive balance sheets with asset sizes around $1.5 trillion, yet their operational focuses diverge significantly.

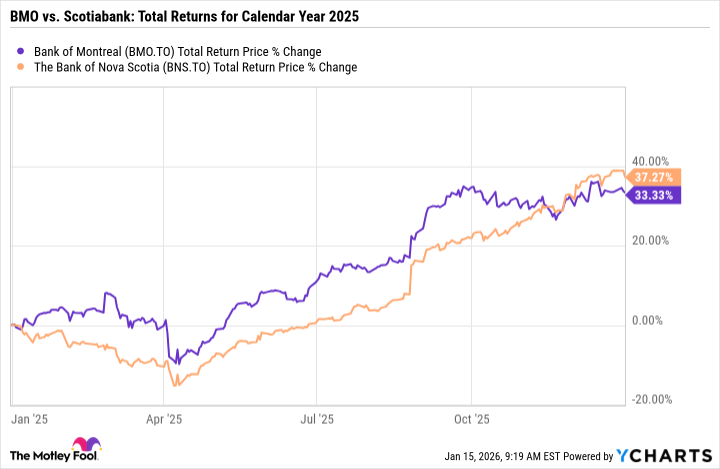

Respective investment return performances from 2025 tell a surprising story. Scotiabank stock managed to narrowly beat BMO stock with a total return of 37.8% compared to BMO’s 33.3% during the past calendar year.

BMO Total Return Price data by YCharts

This outperformance occurred despite Scotiabank suffering massive write-downs early in the year as it exited risky Central American markets. In fact, Scotiabank closed 2025 with significant momentum, posting a 12-month return of 45.2%, far outpacing BMO’s 37.6%.

If you’re looking to position your portfolio for the next decade, here are three key points to help you decide which Canadian bank stock is the better buy today.

Source: Getty Images

Geographic exposure in 2026: The U.S. vs. The Americas

The most critical difference between these two lenders lies in where they generate their profits.

Bank of Montreal has bet the farm on the United States. In 2025, BMO generated 41% of its adjusted earnings from south of the border, with the majority 59% coming from Canada. This makes BMO a true North-South play, offering investors direct exposure to the American economy and the strength of the U.S. dollar without leaving the TSX.

Scotiabank is taking a more diversified approach. While it is pivoting toward a “North American Corridor” strategy, its earnings mix remains complex. In the last quarter, it generated 48% of net income from Canada, 16% from the U.S., 9% from Mexico, 11% from the Caribbean, and 16% from other markets. Although the bank is exiting volatile regions, a significant portion of its net income still flows from emerging economies. This exposure adds a layer of geopolitical risk but also offers higher potential growth rates than the saturated Canadian and U.S. markets.

Yields and valuation

Scotiabank trades at a forward price-to-earnings (P/E) ratio of 12.3, making it visibly cheaper than BMO stock, which trades at a forward P/E of 13.1. The market continues to discount Scotiabank shares due to the complexity of its international footprint, but this gap provides a margin of safety for new buyers in 2026.

The dividend income story is equally compelling. Scotiabank stock offers a superior dividend yield of 4.3% for 2026, which sits a full 70 basis points higher than BMO’s 3.6% yield. If you are a passive income seeker relying on portfolio cash flow, that difference can be substantial.

Most noteworthy, both banks remain adequately capitalized to support these payouts, with BMO reporting a common equity tier-1 (CET1) ratio of 13.3% and Scotiabank close behind at 13.2%.

BMO vs. Scotiabank stock: The wealth management wild card

One often overlooked earnings growth catalyst is the sheer scale of Scotiabank’s wealth management operations.

While BMO is known for its commercial banking prowess, Scotiabank is a giant in wealth management. It boasts a massive portfolio with $797 billion in assets under advisory (AUA), dwarfing BMO’s $282 billion. Furthermore, Scotiabank holds $432 billion in assets under management (AUM) compared to BMO’s $390 billion.

This scale matters because wealth management is a capital-light, high-fee business. Scotiabank simply has more assets upon which to earn future commissions and management fees than BMO does. If the global capital markets perform well in 2026, this segment could be a powerful earnings driver for Scotiabank. The bank is also counting on the growing middle class in its emerging markets to become new wealth management clients, providing a long-term growth runway that BMO stock may lack.

The Foolish bottom-line

So, which Canadian bank stock should belong in your portfolio?

If you want a simpler, lower-risk business model with heavy exposure to the U.S. economy, Bank of Montreal stock is the solid choice. It is a consistent operator with a clearly defined growth lane.

However, if you are willing to accept slightly more complexity (risk) for higher potential rewards, Bank of Nova Scotia stock appears to be the better bargain. It offers a higher yield, a cheaper valuation, and significant upside if its wealth management strategy pays off. With operations expanding in the less-volatile U.S. market and strong share-price momentum behind it, Scotiabank stock looks poised to continue its recovery this year.