Canadian telecom sector giant TELUS (TSX:T) stock offers a jaw-dropping 9.9% annual dividend yield. That’s more than double the 4.4% you’d get from Rogers Communications (TSX:RCI.B) and nearly double BCE (TSX:BCE) stock’s 5.3% payout.

But here’s the catch: TELUS paused its semi-annual dividend growth policy back in December 2025. The quarterly payout remains stuck at $0.4184 per share and could stay flat all the way through 2027. For passive income investors, that’s a worrying signal. What if management decides to cut the juicy payout so the yield falls towards “current industry norms”?.

So, is the payout still worth counting on for passive income purposes? Let’s break down the risks – and the reasons for hope.

Source: Getty Images

What threatens TELUS’s dividend?

After a period of heavy capital spending, TELUS exited 2025 with a net-debt-to-EBITDA (adjusted earnings before interest, taxes, depreciation and amortization) ratio of 3.4 times – elevated by historical standards. If interest rates climb again before the company successfully deleverages, interest costs could surge, squeezing distributable cash flow.

Worse, wireless average revenue per user (ARPU) keeps declining thanks to fierce price competition. During the fourth quarter of 2025, adjusted net income fell 18.4% year over year. Based on earnings, TELUS stock’s dividend consumes more than 100% of normalized earnings.

But here’s the twist: because TELUS carries expensive telecom equipment on its balance sheet, leading to heavy depreciation and amortization charges, the earnings payout ratio isn’t the right metric to watch. Investors should watch cash flow instead.

Three reasons TELUS stock’s dividend will survive

TELUS stock’s dividend may easily survive a chop because the company is growing its free cash flow (FCF), its revenue base is still steadily growing in the low single digits, and management is working on strengthening the balance sheet through debt repayments.

Free cash flow is king. It basically measures the discretionary cash from operations, after sustaining capital expenditures. Management may choose to use free cash flow to pay down debt, reinvest to grow the business, or to reward shareholders through dividends and share repurchases.

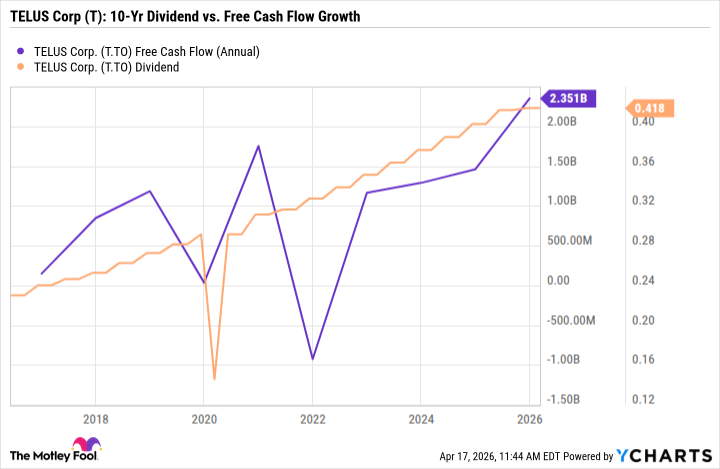

TELUS reported record FCF growth in 2025, up 11% year over year. Management targets 10% annual FCF growth through 2028, which would sustain a recent trend and comfortably cover the dividend. Lower capital spending in 2026 means more operating cash flow to service the dividend payout.

T Free Cash Flow (Annual) data by YCharts

TELUS’s revenue keeps growing. Canadian population growth, steady adoption of TELUS Digital, and client wins are driving top-line expansion. Potentially growing contributions from TELUS International also diversify cash flow.

Most noteworthy, deleveraging is underway. Real estate monetization and non-core infrastructure sales will help pay down debt and reduce interest expenses. Interestingly, TELUS already boasts the strongest balance sheet among Canada’s Big Three telecoms:

| Company | Net-Debt-to-Adjusted EBITDA | Recent trajectory |

| TELUS (TSX:T) | 3.4x | Falling from 3.9x in 2024 toward a 3.3x target for 2026 |

| Rogers (TSX:RCI.B) | 3.9x | Recovered quickly from near 5x post-Shaw merger in 2023. |

| BCE (TSX:BCE) | 3.7x | Still elevated, legacy revenue weaknesses |

Investor takeaway: FCF vs. debt argument

TELUS stock has the cash flow capacity to sustain its dividend at current levels. Management’s payout ratio guideline of 60% to 75% of free cash flow should be achievable going forward.

But the market’s skepticism is still baked right into that 9.9% yield. Investors are clearly worried about the debt. Progress on repayment will be the single most critical factor to watch.

If interest rates start rising again before TELUS hits its deleveraging targets, management may prioritize debt reduction over the dividend. And that could mean a cut.

A near-10% payout is never a free lunch. This one still comes with real risk, but for patient investors willing to monitor the balance sheet, TELUS’s dividend may just survive.