Building a bulletproof Tax-Free Savings Account (TFSA) portfolio naturally takes some time and commitment on the investor’s part. Some aspirational growth investments may take a while to shoot off. So balancing them with some income-generating assets could prove desirable as you wait for your growth stocks to gain compounding momentum. Dividend-paying stocks that drop regular paycheques into a registered investment account come in handy, and CT Real Estate Investment Trust (TSX:CRT.UN) is one of the ideal TFSA stocks to buy and hold for consistent passive income.

Source: Getty Images

CT REIT: An ideal TFSA stock

Around the 15th of every month, CT REIT distributes a portion of rental income generated from a portfolio of 375 predominantly retail properties totalling 31.7 million square feet of gross leasable area (GLA). The payout currently yields 5.3% annually. In a TFSA, that regular, constant, and consistent passive income stream is desirable. You could diversify into new stakes in other dividend stocks, snag some shares in exchange traded funds (ETFs), or pay some of your recurring living expenses with it.

But what confidence can new investors have in CT REIT’s ability to pay constant cash into TFSA accounts? Let’s talk more about that.

The Canadian REIT runs a resilient real estate business model inherited from parent and major tenant Canadian Tire Corporation, an investment-grade rated convenience store chain that’s expanding its footprint.

The ultimate investment-grade anchor

The single biggest risk facing Canadian REITs is usually portfolio vacancy. If tenants hit economic headwinds and fail to pay rent, landlords may have to slash distributions. However, CT REIT possesses a structural competitive advantage that its retail peers can only dream of: its relationship with Canadian Tire Corporation.

Canadian Tire isn’t just CT REIT’s anchor tenant; it is its controlling shareholder and a highly stable, investment-grade credit-rated retail behemoth that’s unlikely to fall behind on rental payments any time soon. This strategic alignment keeps CT REIT’s nationwide portfolio essentially fully leased. The REIT’s portfolio is essentially fully leased with a 99.4% occupancy rate going into the second quarter of 2026.

A fairly long weighted average lease term of 7 years implies strong revenue and cash flow visibility for the trust.

As Canadian Tire continues to modernize and expand its digital and physical retail footprint, CT REIT enjoys a highly visible, locked-in pipeline of rental revenue.

Built on an ironclad balance sheet

In a higher-for-longer interest rate environment, excessive leverage can quietly destroy equity values. Fortunately, CT REIT has played defence beautifully over the years. The trust wrapped up the first quarter of 2026 maintaining a remarkably low debt ratio of just 39%.

This conservative leverage insulates the REIT against refinancing volatility and leaves ample liquidity to fund high-margin development projects without aggressively diluting its unitholders.

CT REIT’s massive payout margin of safety

A high dividend yield is a trap if the underlying cash flows can barely sustain it. CT REIT’s 5.3% distribution has a stellar margin of safety, as shown by its Adjusted Funds From Operations (AFFO) payout ratio of just 72.5% during the first quarter.

By retaining more than 27% of its recurring distributable cash flow, the trust secures a two-fold advantage. First, the monthly distribution is virtually bulletproof against unexpected operational pressures. Second, it retains a significant internal cash pile to organically compound growth through developments, meaning the REIT’s distribution has clear potential to sustain a multi-year growth runway.

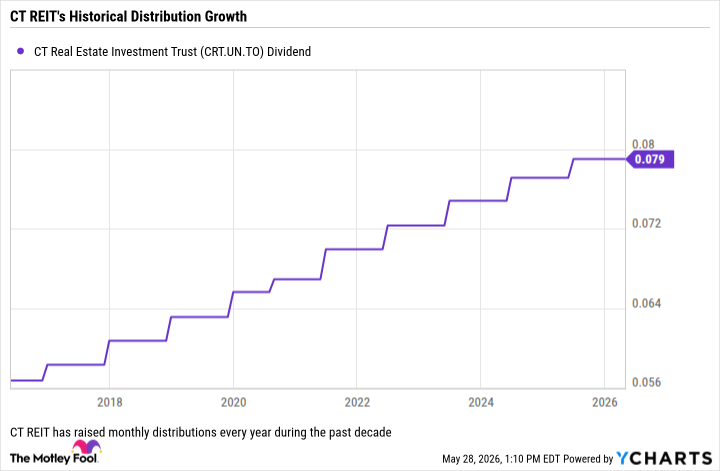

A decade of reliable dividend hikes

True wealth building requires income growth that outpaces inflation. CT REIT hits this mark flawlessly. Since its initial public offering in 2013, the REIT has increased its distribution every single year, raising its payout by approximately 50% over that span.

CRT.UN Dividend data by YCharts

A small portion of the distribution (7.8% for 2025) is usually Return of Capital (ROC) while more than 90% is usually taxable income, with the remainder treated as capital gains. Rather than navigating the complex tax treatment of such classifications REIT distributions typically face in standard non-registered accounts, shelter the entire payout in a TFSA.

By utilizing your TFSA as the holding account for CT REIT units, you ensure that every single monthly cash distribution bypasses the tax collector entirely.