- What is an exchange-traded fund (ETF)?

- What is a mutual fund?

- How are ETFs and mutual funds similar?

- 1. They’re both overseen by fund managers

- 2. They both help you diversify

- 3. They both have expense ratios

- How are ETFs and mutual funds different?

- Mutual funds vs. ETFs: Which is right for you?

- Choose an ETF if you want …

- Choose a mutual fund if you want …

Every savvy investor knows investing in a fund is hands-down one of the best ways to diversify your portfolio. But which is better: a mutual fund or an exchange-traded fund (ETF)?

Sure, both mutual funds and ETFs give you broad market exposure at an affordable cost. But beyond diversification, ETFs and mutual funds have profound structural differences that affect how you buy and sell them, how much you pay in taxes, and how much you’ll owe in fees.

Let’s look closer at mutual funds and exchange-traded funds to see which one better fits your investing strategy.

What is an exchange-traded fund (ETF)?

An exchange-traded fund (ETF) is a basket of investments (such as stocks, bonds, or commodities) that you can buy or sell during normal trading hours. ETFs usually follow an index, such as the S&P/TSX Composite Index, and may track certain industry sectors (e.g., gold, semiconductors), countries (e.g., China, France), or regions (e.g., Asia, Latin America).

| Pros | Cons |

| Trading flexibility. ETFs can be bought and sold during normal trading hours. | More frequent commission charges. Like stocks, you’ll pay a commission to a broker whenever you trade an ETF. |

| Increased diversification. One share could spread your money across numerous companies or market sectors. | Little opportunity to beat the market. Passively managed ETFs track the market, but never surpass it. |

| Lower overall cost. Compared with mutual funds, ETFs are surprisingly cheap. | No control over stock picks. The fund manager decides which stocks to invest in (a “pro” or even robo picks stocks for you!) |

RELATED: Best Canadian Dividend ETFs

What is a mutual fund?

A mutual fund is an actively or passively managed basket of investments that you can buy or sell at the end of the trading day (more on this below). Mutual funds give investors the chance to pool their money together and buy stocks, bonds, and other assets in multiple companies.

| Pros | Cons |

| Actively managed. A professional will research, pick, and monitor the performance of the underlying stocks. Like ETFs, passive mutual funds track an index and thus charge lower fees. | More expensive than ETFs. The expense ratios can be very high. Even the fees for a passive mutual fund tend be higher than those of an ETF. Plus, you’ll pay numerous additional fees. |

| Instant diversification. Investing in a mutual fund can help you spread your money across numerous stocks. | Trades only at the end of market hours. You can’t trade frequently during the day, only when the market closes. |

| Potentially outperform the market. Active mutual fund managers don’t track a market index; they’re trying to beat it. | Less tax efficient. The active buying and selling of shares within a fund can produce higher capital gains taxes. |

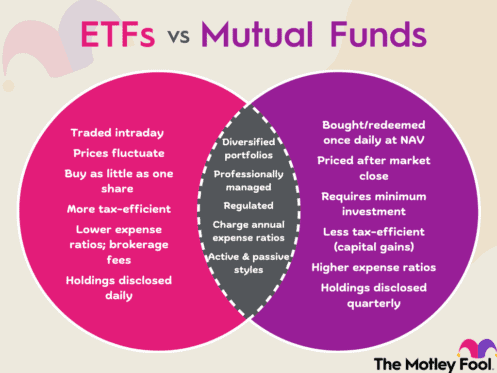

How are ETFs and mutual funds similar?

As you can see, ETFs and mutual funds aren’t worlds apart. In fact, ETFs and mutual funds were created to solve a similar problem: how to help hands-on investors diversify their portfolios without the pain of hand-picking investments themselves.

For that reason they share many traits, including the following.

| ETFs | Mutual funds | |

| Are they overseen by a fund manager? | ✅ | ✅ |

| Do they provide more diversification than stocks? | ✅ | ✅ |

| Do they have expense ratios? | ✅ | ✅ |

1. They’re both overseen by fund managers

Every fund has a fund manager, someone who oversees its performance, rebalances it, and ensures it hits its investment objectives. Fund managers also own the investments inside the fund: when you invest with one, you own a share of the fund, but not the investments themselves.

2. They both help you diversify

Both ETFs and mutual funds allow you to invest in a broad range of companies, some of which you probably wouldn’t have known of beforehand. If you don’t have time to pick individual stocks, ETFs, and mutual funds can give you market exposure at a lower cost.

3. They both have expense ratios

As great as a diversified basket of investments sounds, they’re not free: you’ll pay an expense ratio to own them. The expense ratio is simply all the annual operating fees in a fund expressed as a percentage. For instance, if you bought a mutual fund with a 1% expense ratio, you’d pay $10 a year for every $1000 you invest.

How are ETFs and mutual funds different?

Mutual funds have been around since the 1920s, and they’ve survived a great depression, two world wars, and enough recessions and corrections to make even Warren Buffet break a sweat. ETFs are younger (circa the 90s), but their quick rise to fame has given mutual funds a run for their money. Here’s how the two funds are different.

| ETFs | Mutual funds | |

| How are they traded? | Intraday. Like stocks, you can trade ETFs as much as you like during normal market hours. | Once per day. You can place an order to trade a mutual fund during market hours, but the trade won’t be executed until the exchange closes. |

| How much do they cost? | Trading commissions to your broker + the expense ratio to the ETF provider. The fees on ETFs are typically very low compared to those of mutual funds. | Expense ratios + other fees (such as sales loads, back-end loads, or purchase fees). Mutual funds are usually more expensive than ETFs. |

| Do you need a minimum investment? | Low. Investors can buy one share or a fraction of one. | High. Investors may be required to buy a specific number of shares, or invest a certain amount of money upfront. |

| Are they passively or actively managed? | Passively managed. ETFs track a market index but do not actively beat it. | Actively or passively managed. The active fund manager will try to outperform the overall market. |

| Are they tax efficient? | You pay capital gains taxes when you sell your ETF on an exchange for a gain. | You pay capital gains taxes when the fund manager sells an underlying security for a profit. Since this can happen frequently, mutual funds are typically less tax efficient than ETFs. |

RELATED: Active vs. Passive Investing: Which is Right for You?

Mutual funds vs. ETFs: Which is right for you?

Choosing if an ETF or mutual fund is right for you is a personal decision. Here’s how to decide which fits your situation best.

Choose an ETF if you want …

- To “set it and forget it.” Long-term investors who do not want to stock pick, enjoy diversification and low fees when they buy and hold ETFs.

- More trading flexibility. If you’re an active trader, an ETF may also be right for you. You can also employ different short-term trading strategies with them, such as stop orders, short selling, and limit orders.

- Lower capital gains taxes. Generally speaking, ETFs are more tax efficient than mutual funds.

- Fewer (and lower) fees. You’ll pay less in fees when you invest in an ETF. Not only that but your expense ratio will likely be lower than a mutual fund’s. Just be careful of commission creep: every trade you make means you’ll pay a trading commission, which can start to add up.

Choose a mutual fund if you want …

- The potential to outperform the market. It’s not guaranteed your mutual fund manager will beat the market. But if you want that opportunity, a mutual fund might be right for you.

- An actively managed investment. Active mutual fund managers will buy and sell stocks as they see fit. This could expose you to higher-performing investments.

- To “set it and forget it.” Both active and passive mutual funds are suitable for investors who aren’t interested in intraday or day trading.