As an essential business, the stability of the grocery chain business has been prominent through the pandemic. This may be why Loblaw (TSX:L) stock commands a premium long-term normal valuation. Since 2008, this price-to-earnings ratio (P/E) has stood at approximately 16.1.

At writing, the defensive stock appears to be expensive, trading at about 19.2 times earnings at $112 and change per share. However, on closer look, it’s because recent earnings growth has ticked up and is expected to stay relatively high this year and next year.

Grocery stores are a high-volume, low-margin business. As the leader in the space, Loblaw enjoys economies of scale. Its annual revenue has reached $53 billion. Its peers’ revenues are $28 billion for Empire and $18 billion for Metro. However, Metro has been the best well-run company in terms of posting higher margins.

Loblaw, Empire, and Metro Operating Margin (TTM) data by YCharts

Although Metro’s return on assets has been higher, Loblaw took the lead in posting a higher return on equity recently.

Loblaw, Empire, and Metro Return on Assets data by YCharts

Loblaw stock Q1 2022 results

Loblaw reported its first-quarter (Q1) 2022 financial results yesterday. As hinted by its price appreciation in the last 12 months, this quarter, Loblaw benefited from “higher than normal eat-at-home levels.” Perhaps, it’s due to inflationary pressures — eating at home is still cheaper than eating out — as well as some people still being cautious regarding COVID and choosing to eat at home instead of going to restaurants or cafes. Loblaw also noted its Drug Retail business showed strong results with margin expansion.

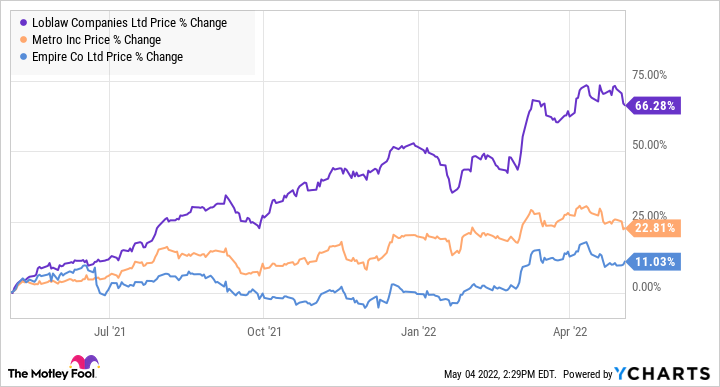

Loblaw, Empire, and Metro stock price data by YCharts

Here are some key highlights of the Q1 2022 results:

- Revenue growth of 3.3% to $12.3 billion

- Retail sales rose 3.2% to $12.0 billion

- Food Retail same-store sales growth of 2.1%

- Drug Retail (i.e., Shoppers Drug Mart) same-store sales increased by 5.2%

- The Retail segment adjusted gross profit rate was 31.1%, up 0.80%

- Operating income rose 19.6% to $738 million

- Adjusted EBITDA, a cash flow proxy, increased by 10.3% to $1,343 million

- Adjusted earnings per share increased by 20.4% to $1.36, which was helped partly by stock buybacks

Valuation and dividend

As mentioned earlier, Loblaw stock is trading at relatively high valuations versus its long-term normal P/E. However, the defensive stock could maintain this relatively high P/E over the next few years with the expectation that inflation will be higher than the last few years. Therefore, the stock is considered to be fairly valued. Yahoo Finance shows the 12-month analyst consensus price target of $119.20.

Loblaw provides a safe yield of approximately 1.3%. It is a Canadian Dividend Aristocrat that has increased its dividend every year since 2012. Its five-year dividend-growth rate is 6.3%. Last year, it increased its dividend by 9.4%. Its 2022 payout ratio is estimated to be about 24% of earnings. Given the higher inflationary environment, it’s possible for Loblaw stock to increase its dividend at a higher rate (roughly 9% per year) over the next few years.

Foolish investor takeaway

Because Loblaw is an essential business, it’s a solid stock for conservative investors to consider. Notably, the defensive stock is, at best, fairly valued. However, it could still be a satisfactory investment over the next few years, as it should continue to do well in a higher inflationary scenario.