Canadians love their bank stocks – and it’s easy to see why. They’re reliable, profitable, and have a history of steady dividend growth. By extension, Canadian investors also love bank exchange-traded funds (ETFs).

There’s no shortage of options here. You can find equal-weight bank ETFs, mean-reversion bank ETFs, yield-weighted bank ETFs, dividend-growth-weighted bank ETFs, and even covered call bank ETFs designed for higher monthly income at the cost of capped upside.

But none of these are my pick for a growth-focused, long-term buy-and-hold investment. For that, I prefer a leveraged bank ETF. If you’re gonna go big, go for broke right?

Now, I know what you’re thinking: “Leveraged bank ETFs are risky! They’re only suitable for short-term trading!” You’re not wrong – most leveraged ETFs are geared for day trading. However, this ETF isn’t like the typical leveraged offerings. Here’s why it’s worth considering.

Source: Getty Images

What makes these ETFs different

When Canadian investors hear “leveraged ETFs,” they usually think of the classic 2 times products designed to multiply the daily performance of an index by two. For example, a 2 times leveraged Canadian bank ETF would theoretically rise 2% on a day when its underlying index gains 1% – and drop 2% if the index falls 1%.

The problem? These ETFs reset their leverage daily, meaning the compounding effect over time becomes unpredictable. That’s because they rely on derivatives called swaps to achieve their leverage. While fine for day trading, holding these ETFs long term can lead to significant performance divergence from the underlying.

The new generation of leveraged ETFs, however, solves this issue. They don’t use swaps or reset daily. Instead, they take a straightforward approach – borrowing money, similar to a margin loan, to amplify exposure. With leverage capped at a manageable 1.25 times, these ETFs provide a more stable option for long-term investors.

The leveraged bank ETF to watch

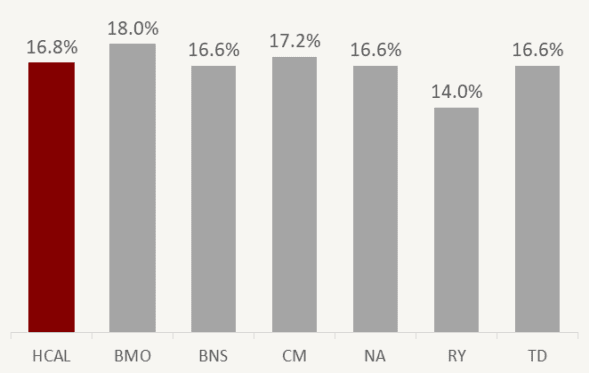

The leveraged bank ETF I like is the Hamilton Enhanced Canadian Bank ETF (TSX:HCAL).

HCAL takes a portfolio of Canada’s Big Six banks, as represented by the Solactive Equal Weight Canada Banks Index, and applies 1.25 times leverage to it. Unlike traditional leveraged ETFs, HCAL doesn’t use swaps or derivatives. Instead, it employs cash margin at institutional borrowing rates to amplify its exposure.

The result? Amplified risk and return, but also a boost in yield. With roughly 25% more dividends than a standard bank ETF, HCAL offers a 6% distribution yield as of Dec. 12, 2024.

While you can expect more pronounced annual volatility compared to a non-leveraged bank ETF, it’s roughly in line with the ups and downs of individual Big Six banks.

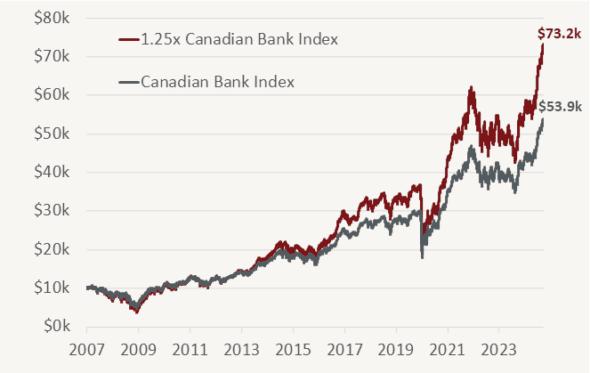

Historically, holding 1.25 times leveraged Canadian bank exposure long enough has also delivered superior returns compared to regular bank investments.