If you are turning 40 and your retirement savings feel nonexistent, you are not alone, and you are certainly not out of time.

The narrative that “it’s too late” is dangerous because it leads to inaction. The reality? Your 40s are often your peak earning years. And you have a 20- to 25-year runway before reaching the traditional retirement age. That’s a lifetime in the stock market.

Whether you’re someone who prioritized paying down debt or you are a newcomer to Canada starting fresh, 2026 is your year to pivot. Here is how to take a $10,000 seed and grow it into a respectable nest egg using a simple “Core and Satellite” investment strategy.

Source: Getty Images

A retirement plan reality check for a 40-year-old

The median Registered Retirement Savings Plan (RRSP) balance for Canadians aged 35-44 was around the $33,000 mark by 2023, though averages (skewed by the wealthy) can look higher.

If you have $10,000 ready to deploy, you are already within striking distance of your peers. The difference is that you are about to implement a strategy that many of them may be lacking.

The strategy: Core and explore

To catch up on your retirement portfolio objectives, you can’t afford to be reckless, but you also can’t be passive. A Core and Satellite retirement plan investment approach strikes this balance. You devote a majority of your money into a reliable “core” made up of cheap index exchange-traded funds (ETFs), and the remainder into high-growth “Satellite” single high-conviction stocks.

Setting up your core portfolio

Your core portfolio is your foundation, and should ideally track the broad market for ultimate diversification. This is your safety net.

iShares S&P/TSX 60 Index ETF (TSX:XIU) is a staple. It gives you low-cost exposure to the 60 largest blue-chip stocks in Canada, including your chartered banks, energy giants, railway stocks, and cash flow secure utilities. XIU ETF offers wealth stability, steady capital gains, and current income. Currently, it yields a dividend of roughly 2.6%.

Over the past decade, XIU has delivered an annualized total return of approximately 12.4%. Even if it reverts to a more conservative 9% historic average, it remains a powerful wealth compounding engine.

Choosing the satellites: Your retirement plan’s growth boosters

This is where you take calculated risks to potentially accelerate your returns. These are individual stocks that you believe will significantly outperform the broader market.

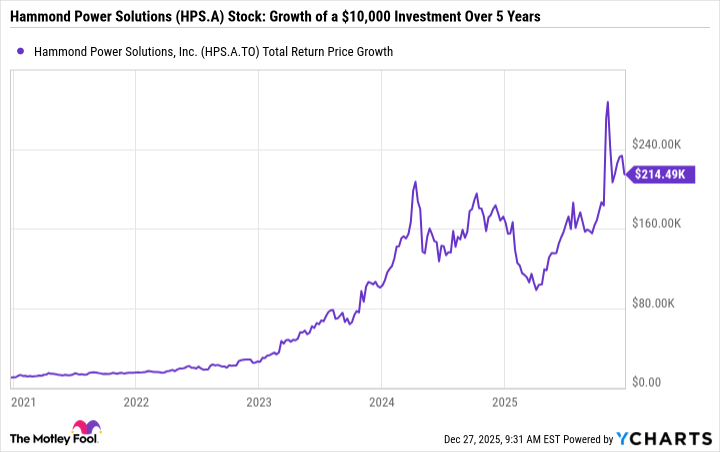

For example, Hammond Power Solutions (TSX:HPS.A) is one electrification stock that could have been a classic satellite pick over the past half-decade as it entered a double-digit revenue and earnings growth spree when global demand for grid expansion and modernization equipment soared. Investors who picked Hammond Power Solutions stock five years ago could be sitting on more than 1,700% in total returns on investment today. A $10,000 investment in the growth stock could be worth $180,000 today, with dividends reinvested.

HPS.A Total Return Price data by YCharts

Past performance isn’t indicative of future returns. However, Hammond Power stock enters 2026 with positive momentum after data centre-related order wins during the fourth quarter increased its backlog by 53%, amplifying its revenue growth potential.

That said, your satellite stock picks require deep research. Joining an investment forum managed by professional stock pickers may help uncover growth stocks that may propel your retirement plan’s growth.

How a $10,000 initial investment could grow in a retirement plan

Suppose you invest your $10,000 today into a balanced portfolio that averages a conservative 9% annual return.

Without any further plan contributions, your $10,000 initial investment may grow to about $86,000 in 25 years (at age 65). That’s not bad, but its not enough a retirement fund.

To create a sizeable retirement plan portfolio, you should commit to regular capital contributions to the plan. Adding $500 a month to the retirement plan, earning 9% annual returns, could build a $625,000 retirement portfolio in 25 years. Fired-up individual stock picks (the satellites) could propel this retirement plan’s growth towards a million and beyond.

The Foolish bottom line

At 40, you possibly have the income to save and the wisdom to stay the course on a retirement plan. Use your Tax-Free Savings Account and Registered Retirement Savings Plan contribution room to optimize tax efficiency, and consider joining reputable investment communities to sharpen your stock-picking skills for those “satellite” positions.

The year 2026 could be the beginning of your retirement plan’s compound growth story. Make it count.