Some stock market investment decisions keep you up at night. This isn’t one of them.

If I could pick just one exchange-traded fund (ETF) to anchor my portfolio for the next three decades, without second-guessing myself, it would be the iShares Core MSCI Canadian Quality Dividend Index ETF (TSX:XDIV). Here’s why this low-cost, passively managed, monthly-income producing index fund has earned my conviction as a core holding in a retirement portfolio.

Source: Getty Images

Best Canadian ETF to buy

The iShares Core MSCI Canadian Quality Dividend Index ETF is one of my best ETFs to buy for long-term holding. It’s $5 billion portfolio hunts for the best dividend stocks on the TSX. Its underlying index, the MSCI Canada High Dividend Yield 10% Security Capped Index, rigorously screens stocks for high quality dividend stocks using criteria such as return on equity, earnings stability, and debt-to-equity ratios that portray strong balance sheets. Only about 21 Canadian blue-chips make the cut, and they’re among the fittest dividend payers in Canada.

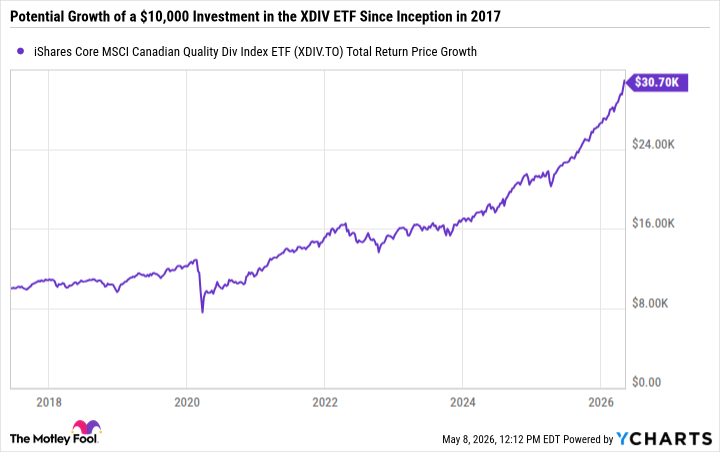

That quality-first approach has been rewarded. Since its launch in June 2017, the XDIV has delivered an annualized total return of roughly 13.6% to reward investors with a 210% total gain on investment. For a portfolio that collects dividends along the way, a double-digit compound annual growth rate is exceptional.

A $10,000 investment in the XDIV ETF at inception in 2017 could have grown to more than $30,000, with dividend reinvestment.

XDIV Total Return Price data by YCharts

A significantly low management expense ratio (MER) of $0.11% (or $1.10 per annum per every $1,000 invested) means investors get to keep most of the investment returns generated by the portfolio. They won’t lose much value to ETF management fees and expenses.

On top of hefty capital gains potential, investors in the XDIV ETF receive a dividend every single month. The most recent monthly dividend should yield a respectable 3.4% annually.

Where could future growth come from?

Skeptics might say past performance doesn’t guarantee future returns, and they’d be right. But the ETF’s design makes tomorrow’s growth potential equally plausible. Its concentrated holdings sit at the intersection of Canadian economic resilience and global demand. These include top-tier banks with fortress balance sheets, pipelines that form the backbone of North American energy, and utility giants that earn regulated, predictable economic returns through economic cycles.

If interest rates drift lower over the next cycle, yield-oriented assets should enjoy a valuation tailwind. Meanwhile, these large-cap, wide-moat companies keep growing their earnings and free cash flow.

Most noteworthy, the XDIV ETF’s passive rebalancing means investors won’t have to guess which pipeline or bank will win. Investors simply own the strongest TSX dividend stocks at all times.

A monthly income ETF you can depend on

The XDIV ETF pays a monthly dividend that yields about 3.4%. The yield appears better than the iShares Core S&P/TSX Capped Composite Index ETF‘s 2%, giving investors a meaningful bump in immediate cash flow. But what excites me more is the growth potential in those monthly payouts.

The monthly dividend ETF’s underlying holdings are stocks that have raised dividends through thick and thin. Since 2017, the ETF’s monthly distribution has climbed from roughly $0.07 per share to around $0.12 today. That’s an income raise almost every year, without investors lifting a finger. For a retiree or an income-focused TFSA, that growing monthly cheque feels like pure gold.

Why the XDIV ETF may be a best buy in any core portfolio

The iShares Core MSCI Canadian Quality Dividend Index ETF (XDIV) can form the core of any portfolio, and it is eligible for registered investment accounts.

For a young investor building long-term wealth inside a TFSA, the monthly distributions turbocharge compounding, and the quality screen offers growth without speculative risk.

For a retiree, the growing income stream helps outpace inflation while the low MER keeps withdrawal values high. Even inside an RRSP, where foreign withholding taxes don’t apply, the sheer dependability of the holdings makes it a one-decision portfolio anchor.

Once the core is all set, it’s time to find the high conviction growth and income stocks that fit one’s investment objectives.