Canadian bank stocks don’t usually get investors’ pulses racing. They’re dependable dividend stocks for core holding purposes, yes, but exciting? Not exactly. Yet the Toronto-Dominion Bank (TSX:TD), or TD Bank stock, has been anything but boring so far in 2026.

After a punishing couple of years battling U.S. regulatory caps and restructuring costs, TD is staging one of the most impressive comebacks on the TSX. Under new CEO Raymond Chun, the bank delivered a knockout second-quarter fiscal 2026 performance, posting an adjusted earnings per share (EPS) up 21% year over year, return on equity (ROE) hitting 14.4% (up over 200 basis points), and record revenue in Canadian Personal and Commercial Banking. Management is now on track to outperform its full-year targets.

TD bank raised its quarterly dividend to common stock investors by 3.7% to $1.12 per share in May, up from $1.08. Management has shifted from an annual dividend review to a semi-annual cycle, meaning investors could see two dividend hikes per year going forward. That’s good music to an income investor’s ears.

Source: Getty Images

Why TD stock is a reliable dividend champion

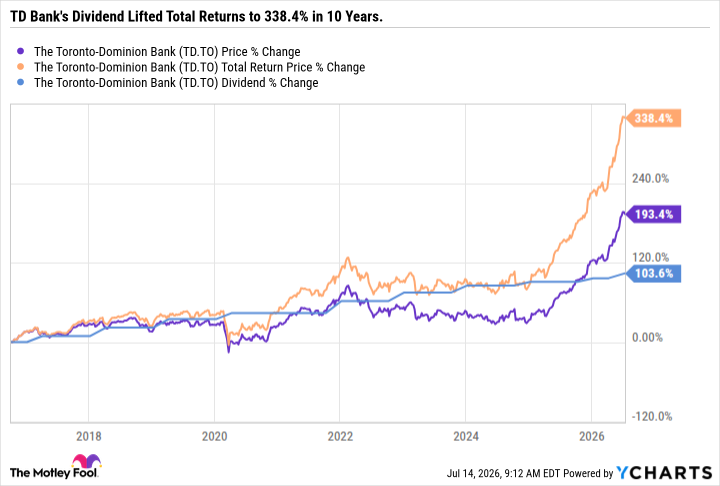

TD Bank initiated dividends way back in the 1850s and has paid uninterrupted quarterly dividends ever since – through economic depressions, recessions, and everything in between. The bank has raised dividends every year since 2011, making it a 15-year dividend growth streak of repute. Over the past decade, the annual dividend has more than doubled, up 103.6%.

The math behind TD stock’s dividend payout is rock-solid. TD’s Common Equity Tier 1 (CET1) capital ratio ended the most recent quarter at 14.3%, well above regulatory requirements. The bank’s $2.1 trillion asset base provides enormous scale and earnings power. With a sustainable payout ratio under 45% and management committed to returning capital through both dividends and aggressive share buybacks, this Canadian bank stock’s regular dividend isn’t going anywhere anytime soon.

The $400 investment: Small money, big potential

TD stock has been historically good for smaller accounts, and if the Canadian economy doesn’t buckle, a core holding investment in the bank’s shares could continue to reward investors with a reliable quarterly dividend stream and potential capital gains.

Trading around $170 per share, a $400 investment budget gets you about 2.3 shares of a premier blue-chip Canadian bank from a brokerage or trading app that allows fractional share trading. That small stake secures an immediate, reliable quarterly payout at a yield of roughly 2.6% – and with the bank now reviewing dividends twice a year, that payout is poised to grow.

Let’s consider the long game. Over the past 10 years, TD stock has delivered a total return (with dividends reinvested) of roughly 338%. Before dividends, capital gains at 193.4% were still respectable.

A $400 investment a decade ago, with dividends reinvested, would be worth approximately $1,754 today. The magic of consistent compounding paired very well with a bank stock that just keeps raising its dividend payout.

A few risks to note

TD’s increased business concentration in Canada means a domestic economic stumble would hit a bit harder. The U.S. asset cap remains a headwind, though management is navigating it well. This isn’t really a risk, but the bank’s current yield is significantly lower than historical averages following an impressive rally. That’s what naturally happens when a stock doubles in little over a year.

Investor takeaway

TD Bank stock has more than doubled since early 2025, but the comeback story is far from over. With double-digit ROE, a fortress-like balance sheet, a dividend that’s survived 169 years of history, and management now reviewing dividends twice annually, this is a reliable dividend stock worth buying, even if you’ve only got $400 to put to work.