Newly listed marijuana producer MedReleaf Corp. (TSX:LEAF) reported a massive jump in year-on-year revenues, but a closer look reveals that the company’s sales actually declined quarter on quarter during the last two quarters.

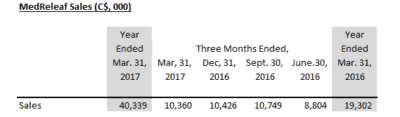

MedReleaf’s reported annual revenues of $40.34 million for the year ended March 31, 2017, which was 109% growth from the $19.3 million recorded in the previous financial year.

However, the company recorded peak revenues of $10.75 million in the quarter ended September 30, 2016, but it never managed to beat this figure in the six months that followed.

In fact, sales declined by 3% in the next quarter that ended December 31, 2016, and went on to shed another 0.6% in the last quarter for a combined 3.6% decline from the peak two quarters ago, as shown below.

A 3.6% drop wouldn’t be a significant figure if MedReleaf was in any other industry, but this is a marijuana producer in a sector where most of the market hype has been for the past few quarters, and sales have declined in an environment where the other guys are growing in leaps and bounds quarter on quarter.

Why would MedReleaf record declining or stagnating quarterly revenues two quarters in a row when others are registering quantum revenue leaps?

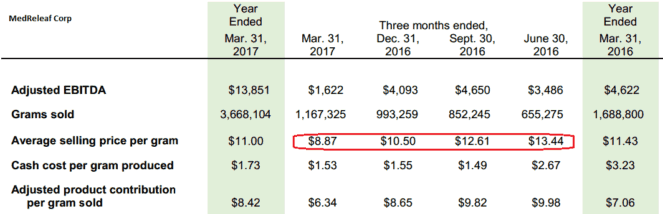

The answer lies in the average price per gram the company has been managing to charge its consumers.

Even though MedReleaf’s product portfolio includes premium-priced oils and premium-priced dried cannabis strains, the company’s ability to maintain higher average prices on its cannabis varieties may be increasingly coming under threat, as the extract below shows.

The management says this trend was caused by the new Veteran Affairs Canada (VAC) Reimbursement Policy for Cannabis for Medical Purposes (the “VAC Policy”), which placed a limit of $8.50 per gram of product effective November 22, 2016. So, the company had to offer discounted prices to qualified veterans.

However, during this same period, Canopy Growth Corp. managed to improve the average selling price per gram, and Aurora Cannabis Inc. registered massive revenue growth rates. Aurora is also popular for its compassionate pricing policy.

Now that the same VAC Policy has increased volume restrictions to a maximum coverage limit of three grams per day effective May 21, 2017, are we going to see further declines in MedReleaf quarterly revenues?

I wouldn’t say so, but MedReleaf needs to grow sales volumes way faster than it is doing now.

The company says it’s assessing the policy’s impact on future profitability, but margins are declining already.

MedReleaf has been negatively affected by the new VAC Policy, but its competitors are not complaining yet; rather, they are recording massive quarter-on-quarter revenue gains.

Foolish bottom line

MedReleaf has enjoyed premium pricing for its product in the past, but the company is losing its pricing power in the market.

The company has waited to embark on expansion programs and has only decided to do so now. It might have been compelled to list publicly in search of the required growth capital after realizing that it may lose ground to the aggressive competition.

However, the company is the most profitable in the nascent industry, and its management deserves credit for that, but I doubt if it has the speed and agility to conquer the recreational cannabis market. Canopy, Aurora, and Aphria Inc. seem much more prepared for this new growth area at this juncture.

Time will tell, and I will be watching closely how MedReleaf will manage to maintain profitability while pursuing its new expansion programs.