Last Friday I wrote about the top two ultra-safe wide-moat stocks in Canada — stable, profitable, companies that could maintain their market share and competitive edge for decades on end.

Since then, I have spent more time hunting for more of these fabled wide-moat stocks, and believe I have stumbled upon a true hidden gem that most Canadian investors are likely unaware of: TMX Group (TSX:X).

Why we want wide moats

For those of you new to the concept, wide-moat stocks are those that can maintain their market dominance over a long period of time. Sources of a wide moat often include things like government protection and bailouts (think utilities), competitive prices and low costs (think e-commerce), or a lack of competition (think of oligopolies like telecom or banks).

We want wide-moat stocks, because they reduce one of the main risks of stock picking: that an individual stock pick can go into decline or even bankruptcy in the long run. We want companies that possess such a durable competitive advantage over time that they can fend off upstart rivals for decades on end and stay profitable.

The widest moat to rule them all

TMX has one of the most overlooked, glaringly large wide moats in the Canadian stock market for a powerful reason: it operates the dominant equities, fixed-income, derivatives, and energy exchanges, most notably the renowned Toronto Stock Exchange (TSX) and the smaller TSX Venture Exchange (TSXV). The company also provides services encompassing listings, trading, and clearing, settling, and depository facilities for Canada (CDS).

TMX has built a tremendously wide moat over the decades. It has established itself as the premier stock exchange for companies looking to go public. The majority of Canada’s stock indexes, including the S&P/TSX 60 and the S&P TSX Capped Composite are drawn from listings on TMX Group’s exchanges.

The smaller exchanges in Canada, such as the Canadian Securities Exchange (CSE) and the Aequitas NEO Exchange (NEO) are unable to compete effectively against TMX’s economy of scale, reputation, and operating model. Any reputable company seeking to go public inevitably uplists to the TSX if they want the best access to capital. Very few large-cap companies choose to remain on the CSE, NEO, or even TSXV.

What the numbers say

As a result of its wide moat, TMX has some excellent fundamentals that point to its profitability, excellent management, and competitiveness. TMX currently has a gross margin of 53.61%, profit margin of 32.27%, and ROE of 8.85%. Quarterly YoY revenue growth stands at 7.60% with quarterly YoY earning growth at 9.90%. The balance sheet is healthy, with $337.9 million in cash for the most recent quarter and a current ratio of 1.01.

Technicals wise, TMX has a beta of 0.62, making it less volatile than the market. As of of December 12, it is currently trading at $125.50, or 15.25% lower than its 52-week high of $145.69. The current price also is lower than both its 50-day and 200-day moving averages of $131.21 and $133.66, respectively, which could indicate further downside potential in the short term.

The Foolish takeaway

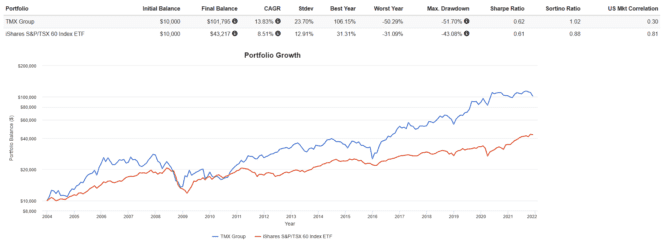

Despite the recent short-term bearish trend, over the long term, TMX has consistently beat the market. Below, I have provided a backtest of $10,000 invested in TMX vs. iShares S&P/TSX 60 Index ETF since 2004 with dividends reinvested from Portfolio Visualizer:

Although TMX has higher volatility (standard deviation of 23.70% vs 12.91%) than the index, it also has a higher return (CAGR of 13.83% vs 8.51%), leading to an overall similar risk-adjusted return (Sharpe ratio of 0.62 vs 0.61).

Although past performance is not indicative of future performance, I think TMX should be able to maintain its wide moat for the foreseeable future. It is unlikely that an upstart exchange can find the network, capital, and influence to disrupt its market share dramatically. If you can stomach the volatility of holding TMX vs the index, it could potentially pay off with better returns.