Sometimes, the best way to build a passive-income-producing family legacy is to simply invest in the established family legacies of others. Power Corporation of Canada (TSX:POW) represents exactly this kind of dividend growth investing opportunity. The thriving holding company has been a Desmarais family legacy since Paul Desmarais acquired a controlling stake in 1968. While the blue-chip stock has been creating wealth for shareholders for a full century since 1925, its modern incarnation is what matters most to investors today.

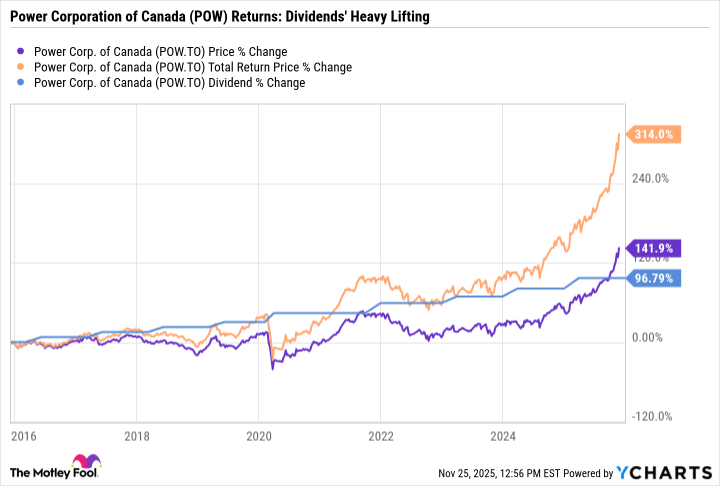

At first glance, Power Corporation of Canada stock might not seem like a high-yield screamer. The conglomerate’s 3.4% dividend yield appears average in the current market environment. However, experienced investors know that current yields are only part of the long-term investing story. The quarterly payout has been the silent engine behind the stock’s impressive 308% total return over the past decade.

Source: Getty Images

Power Corporation’s financial portfolio evolution

The company has evolved significantly from its origins as an electric utility and financier. By the 1970s, it had become a diverse holding company with a smorgasbord of businesses. Today, it is a focused financial services powerhouse. Power Corporation owns major stakes in Great-West Lifeco, IGM Financial, and GBL. It also directly operates distinct alternative asset management businesses, including Sagard and Power Sustainable, while holding stakes in high-growth platforms like Wealthsimple.

Its net-asset-value-based investments have been a driving force for returns lately. For example, the company’s investments in Wealthsimple and Rockefeller Capital Management have seen their fair values grow by 47% and 89%, respectively, this year.

Strategic shifts driving growth

Perhaps the most significant move the Desmarais family made to change the company’s fortunes in the late 1960s was a strategic pivot to restructure, dispose of underperforming holdings, and focus intensely on earnings, revenue and free cash flow growth. This shrewdness and decisiveness remains a core part of the company culture. While the retained name “Power Corporation” still reminds the market of its power-generation-utility or industrial behemoth past, the conglomerate is a nimble financial sector player today that has helped shape the Canadian financial landscape for decades.

The Desmarais legacy has lived on through recessions and economic shocks. It thrives in 2025, and POW stock has rewarded long-term investors with a steady 308% total return during the past decade.

A dividend growth story to buy and hold forever

For loyal shareholders, POW stock’s returns stability has translated into tangible wealth. During the past decade, dividends did the heavy lifting. Power Corporation’s dividends lifted total returns from a 138% capital gain to nearly 308% in total returns.

This is why I view POW as a prime dividend growth stock to buy and hold forever. The company has almost doubled its dividend payout during the past 10 years. For early investors who acquired shares back in 2015, that growth has effectively doubled their yield on cost.

The value in POW stock

The current 3.4% dividend yield might not turn heads immediately, but POW’s management team has been aggressively repurchasing shares and raising dividends to enhance shareholder returns. This strategy was designed to help narrow a conglomerate discount on its common stock, and it has worked perfectly.

The discount has narrowed significantly from double-digit ranges to roughly 2% today. With a Net Asset Value of $72.24 per share as of September 30, 2025, the stock is trading almost exactly at the value of its underlying parts. Power Corporation repurchased 7.4 million shares during the first nine months of this year, worth $382 million, and recently raised its quarterly dividend by 9%.

Building generational wealth

The historical math for long-term holders is compelling. If you had invested $10,000 in Power Corporation stock back in 2015, avoided selling during the pandemic crash of 2020, and reinvested all your dividends, you would have nearly $41,000 in your account today. You would have effectively become rich alongside the Desmarais family members who are still diligently managing their own legacy beyond 2025.

As I said earlier: Sometimes, to build your family’s legacy, you have to invest in the legacies of others.