It appears tamed, but as long as it stays above zero, inflation is the silent thief that wipes away your real purchasing power. This is especially true for long-term income investment portfolios designed to fund a retirement that could last decades. If your income stream stays flat while the cost of living rises, you are effectively taking a pay cut every single year.

The easy solution lies in investing in Canadian dividend stocks that consistently increase their payouts, offering beautiful pay raises that reward patience while protecting your purchasing power. They make dividend investing make sense by amplifying the power of compounding so your wealth grows much faster.

If you are looking for TSX dividend growth stocks for passive income to build a cushion for 2026, these three Canadian heavyweights just raised their dividends in November.

Source: Getty Images

Suncor Energy stock

Integrated energy giant Suncor Energy (TSX:SU) has fully mended its image following the turbulent days of 2020. On November 4, the company raised its quarterly dividend by 5.3% to $0.60 per share. This brings the annualized payout to $2.40, offering a current yield of roughly 3.8% on SU stock.

Suncor has now raised dividends for three consecutive years and appears determined to regain its status in the prestigious S&P/TSX Canadian Dividend Aristocrats Index, perhaps by 2028. Since the 2020 cut, Suncor has aggressively hiked its distribution by 186%, averaging a 10.9% growth rate over the past five years. The payout is now much higher than it ever was in the company’s 44-year history as a dividend stock.

What makes Suncor stock a compelling core holding is its integrated model. Its upgraders and refineries run full throttle to enjoy lower input costs even when oil prices dip. Furthermore, Suncor has direct access to retail and wholesale markets through its massive network of Petro-Canada stations. This allows it to sell finished products without incurring U.S. tariffs, a significant advantage in the current economic climate.

Fortis

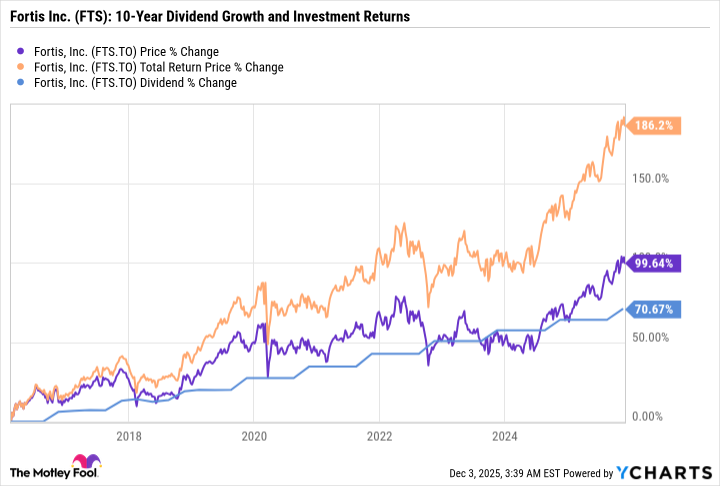

If you want a sleep-well-at-night stock, look no further than Fortis (TSX:FTS). This $37 billion utility giant serves over 3.5 million customers across North America and the Caribbean. On November 4, Fortis raised its quarterly dividend by 4.1%.

This hike cements Fortis stock’s status as a Dividend King, marking 51 consecutive years of dividend increases. For new investors, the stock offers a yield of roughly 3.5%. While that might seem modest compared to high-yielders, the growth story is where the magic happens. Investors who bought Fortis stock a decade ago are now sitting on a 100% capital gain and a total return of nearly 190%.

Looking ahead, Fortis has announced a record $28.8 billion five-year capital investment plan for 2026 through 2030. This plan targets a 7% growth in its rate base, which supports management’s guidance for annual dividend growth of 4% to 6% through 2030.

Fortis pays out less than 75% of its earnings in dividends, ensuring these payouts remain well-covered by stable, regulated cash flows.

TELUS stock

Investors seeking immediate, high-impact passive income could be happy to check out TELUS (TSX:T) stock as it currently offers a staggering 9.2% dividend yield. TELUS maintained its long streak of semi-annual dividend increases by raising its quarterly dividend on November 7 by 0.5% to $0.4184 per share. However, in a recent market update on Wednesday, December 3, TELUS won’t be raising its payouts anymore, until its share price reflects growth prospects.

While the recent 0.5% sequential increase appears symbolic, the payout is up 4% year over year. TELUS had raised dividends for 21 consecutive years, and the announced pause may enable it to grow free cash flow and assist a recovery in its stock price. The best time to lock in a juicy 9.2% dividend yield on TELUS stock could be now, or never. Management has set aside its initial plan to effect annual dividend increases of 3% to 8% through 2028, in favour of 10% annual growth in free cash flow and debt repayments.

Despite the high yield, the current payout remained within management’s acceptable range of 60% to 75% of prospective free cash flow. With free cash flow rising 14.2% last quarter and operational cash flow hitting an eight-quarter high, the dividend looks safe for those seeking substantial dividend yields for passive income.