Enbridge (TSX:ENB) stock is likely a cornerstone investment in many retirement portfolios geared towards passive income. For investors looking to hold the dividend growth stock for the long term, the futuristic question as we look toward 2030 goes beyond ENB stock’s juicy 6.1% dividend yield to focus on the pipelines giant’s strategic pivot. Enbridge is no longer just a “pipeline company”; it is rapidly transforming into North America’s largest natural gas utility and a burgeoning clean energy power player.

Here is what the next five years look like for Enbridge, based on their latest 2026 guidance and long-term strategic outlook.

Source: Getty Images

The forecast: Enbridge by 2030

Management’s most recent guidance for Enbridge targets 5% annual growth in earnings before interest, taxes, depreciation and amortization (EBITDA) and distributable cash flow (DCF) through the end of this decade.

Using Enbridge’s confirmed 2026 guidance as a baseline and applying management 5% compound annual growth rate (CAGR) target, here is a potential financial snapshot for 2030:

| Financial Metric | Guidance for 2026 | Estimated 2030 Value | Comment |

| Adjusted EBITDA | $20.5 billion | $24.9 billion | Based on mid-point of 2026 guidance |

| Distributable Cash Flow (DCF) per Share | $5.90 | $7.17 | Based on mid-point of 2026 guidance |

| Dividend Per Share | $3.88 | $4.72 | Dividend yield (on today’s cost) grows to 7.4%. Payout rate remains sustainable at 66% of DCF. |

The future remains uncertain, and actual results will vary.

The EBITDA growth engine through 2030

Enbridge stock’s revenue, earnings, and cash flow growth engine has shifted gears. While liquids pipelines (oil) remain the cash cow, growth drivers for the next five years include natural gas and renewable energy.

Following massive acquisitions of U.S. gas utilities, Enbridge holds a steady, regulated earnings base in a geographic region experiencing demand growth as power generation utilities respond to growing electricity demand as power-hungry artificial intelligence (AI) data centres sprout. Enbridge’s gas transmission network is within 50 miles of nearly half of its forecasted demand, positioning the company in the vicinity of needy customers.

Moreover, growth in liquefied natural gas (LNG) exports from North America acts as another revenue and earnings growth driver for Enbridge whose infrastructure connects with rapidly growing LNG export facilities on the Gulf Coast.

A stellar 5-year investment plan

Enbridge has moved into a “self-funding” model and may no longer need to issue dilutive equity to grow. The company expects to invest about $10 billion annually without tapping into equity markets.

With a backlog of about $35 billion in secured capital for projects coming online through 2030, Enbridge’s high growth visibility is attractive for long-term investors looking to buy and hold the dividend growth stock beyond 2030.

ENB’s strategic shifts and new risks

Enbridge is diversifying its pipelines business and expanding into a super-energy utility as it aggressively invests in lower-carbon opportunities, including solar farms, offshore wind, and renewable natural gas (RNG), and hydrogen. The new projects may alter its investment risk profile by 2030.

While diversification lowers ENB stock’s carbon risk, it introduces execution risk. Building offshore wind farms and carbon capture hubs could be technically more complex and less proven (for Enbridge) than laying pipelines. Investors should watch out for potential cost overruns in these newer distinct business lines.

ENB stock’s potential investment returns through 2030

Given a 6.1% starting dividend yield for 2026 and a potential dividend growth rate of 3% to 5% annually through 2030, Enbridge stock could be a powerful total return generator over the next five years. The stock offers a potential 11% annual total return profile over the next half decade, holding its valuation multiples constant.

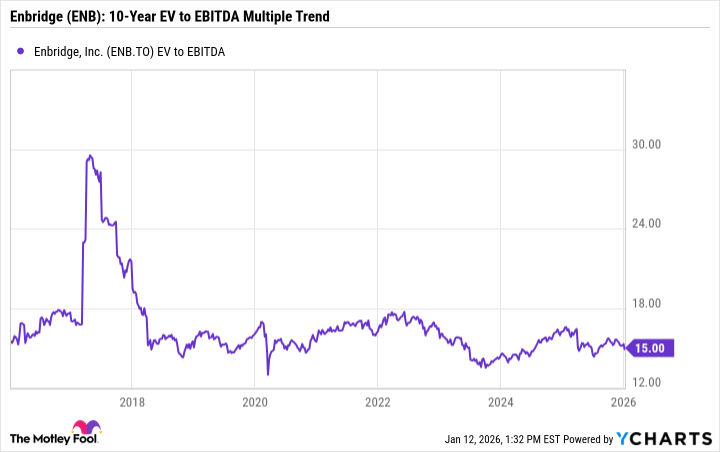

Enbridge’s enterprise value-to-EBITDA (EV to EBITDA) multiple has been range bound since 2018.

ENB EV to EBITDA data by YCharts

While interest rate risks will continue to linger as Enbridge refinances maturing debt obligations, the dividend growth stock appears attractive for new long-term-oriented money right now.

In five years, Enbridge will likely be a larger, and more diversified utility-like stock with strong dividend yields that nourish income seekers’ cash flow cravings.