Imagine getting a dividend raise every year from your investments, paid out monthly, while the underlying business grows stronger and its credit rating improves. That’s the picture forming for Morguard North American Residential REIT (TSX:MRG.UN), a residential landlord with a 4.5% yield that just notched a major credibility upgrade and is steadily marching toward Canadian dividend royalty. If you’re hunting for recurring passive income, this REIT deserves a closer look.

Source: Getty Images

Morguard Residential REIT graduates from high-yield risk to investment-grade stability

The biggest news in April was that Morningstar DBRS upgraded Morguard North American Residential REIT’s credit rating from BB (high) to BBB (low). That may sound like just another notch climb, but here’s the translation: the REIT is no longer a borderline junk-rated borrower. It’s now officially an investment grade debt issuer for the first time.

Why does this matter? An investment-grade status unlocks cheaper, more flexible financing. The REIT can now tap the unsecured debt market on much better terms, funding new developments or acquisitions without significantly diluting unitholders.

This credit rating upgrade didn’t come from luck. The REIT spent the past several years selling roughly $770 million of non-core assets, paying down debt, and laser-focusing its portfolio on multi-suite residential buildings in high-demand markets. That discipline directly strengthens the reliability of the 4.5% dividend you’re collecting every month.

A billion-dollar partnership with TD Asset Management

In February, Morguard and the REIT announced a joint venture with TD Asset Management to build a $1 billion Canadian multi-suite residential portfolio. Critically, Morguard North American Residential REIT will act as the portfolio manager, earning recurring management fees and potential commissions. This arrangement puts the REIT in a capital-light role, collecting fee income that can further support its distribution without saddling the balance sheet. Think of it as a side stream of cash that flows straight into the dividend safety net.

One more raise away from dividend supremacy

Morguard North American Residential REIT has increased its distribution for four consecutive years. If management delivers another raise in 2026, combined with that fresh investment-grade credit rating, the REIT could potentially graduate into the prestigious S&P/TSX Canadian Dividend Aristocrats Index—a club reserved for high-quality Canadian dividend stocks with at least five years of consecutive dividend growth.

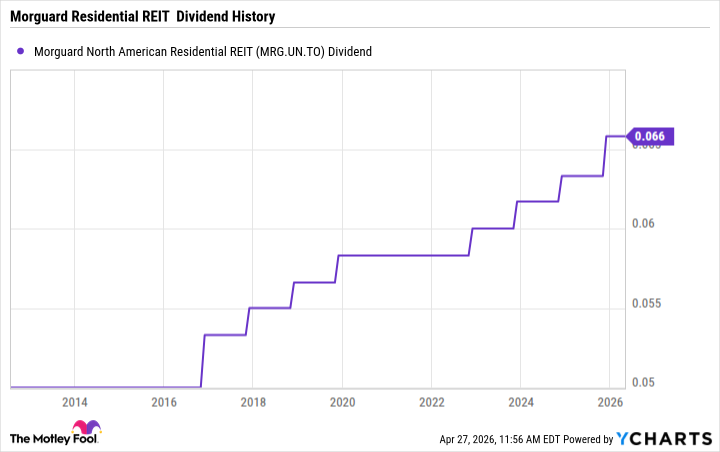

MRG.UN Dividend data by YCharts

Even without the index membership, MRG.UN’s dividend track record is impressive. Since its first payout in 2012, the REIT has never missed a monthly cheque. It has raised its annual dividend in eight of the past 13 years. The current monthly distribution of $0.06583 per unit is backed by a funds from operations (FFO) payout ratio of just 42.7% in 2025, a significant improvement from 45% the year before. That leaves a wide margin of safety, meaning the distribution could keep growing in the near future even as residential rental markets temporarily soften a bit.

Operations strengthening, units undervalued

The residential REIT’s underlying portfolio is performing well, too. In 2025, net operating income climbed 4.6% year over year, and diluted FFO per unit surged 8.5%. Management was so convinced the market mispriced the REIT’s units that it repurchased $24.3 million worth of units at an average price of $17.40. Professionals and insiders saw deep value on the monthly payer’s equity units.

But occupancy dipped in 2025, with Canadian apartments at 93.3% (down from 97.2% at the end of 2024) and U.S. suites closing 2025 at 91.3%. While that warrants monitoring, average monthly rent still rose 4.5% in Canada and 1.2% in the U.S. The REIT expects portfolio economics to stabilize through 2026 as demand for multi-family housing continues to outstrip supply, particularly in its Sun Belt U.S. markets and Alberta.

What to watch now

Morguard North American Residential REIT reports first-quarter 2026 earnings on Tuesday, April 28, with a conference call on May 1. Investors should listen for commentary on rent trends, occupancy recovery, and any hint about the next distribution increase. With a growing, well-covered monthly payout, a freshly minted investment-grade balance sheet, and a clear path toward dividend “aristocracy”, MRG.UN is shaping up to be a compelling monthly income machine for patient Canadian investors.