if you’re looking to build a stream of worry-free passive income, Canadian blue-chip dividend stocks deserve a permanent spot on your buy list. These large-cap Canadian stocks have well-established wide-moat businesses with recession-resistant operations, and management teams that treat dividend growth like a sacred promise. Better still, they hand you a fatter cheque every three months.

When you’re hunting for Canadian blue-chip dividend stocks to buy today, three names stand out: Fortis (TSX:FTS) stock, Canadian National Railway (TSX:CNR) stock, and Pembina Pipeline (TSX:PPL) stock. Here’s why they belong in your TFSA or RRSP.

Source: Getty Images

Fortis

Fortis stock could be an ultimate ‘sleep-well-at-night” dividend stock to buy for decades of growing passive income. The regulated electric and gas utility collects highly predictable income, and its cash flows don’t blink during recessions. High cash flow visibility lets management plan aggressively. Fortis is currently executing a $28.8 billion five-year capital expenditure plan that targets growing its rate base by 7% annually to support 4% to 6% annual dividend increases through 2030.

The FTS stock dividend is well covered. Fortis’s dividend payout ratio has improved sequentially from a peak of 79% in 2021 to a comfortable 70% by 2025. The utility stock has room for another dividend raise later this year.

Fortis has raised its dividends for 52 years, and counting. The most recent 4% dividend bump lifted the annualized payout to $2.56 per share, good for a respectable 3.4% yield today.

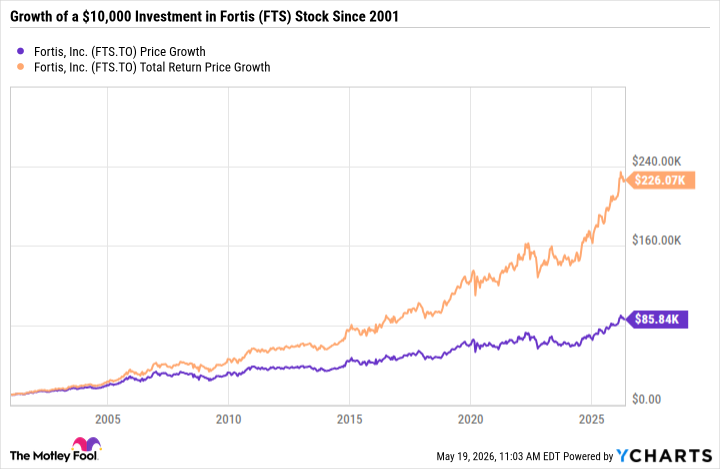

Never overlook what those ever-rising dividends do for total investment returns on the Canadian blue-chip stock. Had you invested $10,000 in FTS stock 25 years ago and reinvested all dividends, your stake would have been worth close to a quarter of a million dollars today. Capital gains only would have lifted the stake to about $85,000.

Canadian National Railway (CNR)

After a three-year lull, Canadian National Railways (CN) stock is roaring back. CNR stock has already delivered about 15% in total returns (dividends plus price appreciation) since the start of the year, and the blue-chip stock is tracing a recovery toward all-time highs.

The railroad stock’s expansive network is an irreplaceable economic artery crisscrossing North America. Competition is scarce – good luck getting the land, permits, and the hundreds of billions needed to build a competing railroad from scratch.

Wide moat businesses like CN command premium valuations, yet today CNR stock trades at a price-to-cash flow (P/CF) multiple of just 13 times, roughly 9% below its five-year historical average.

First quarter results showed strong free cash flow generation (a 44% surge), driven by resilient bulk cargo volumes, while management continues balancing capital spending with dividend raises and share repurchases.

The current CNR quarterly dividend yields 2.4% annually. Management has increased the payout for 30 consecutive years now.

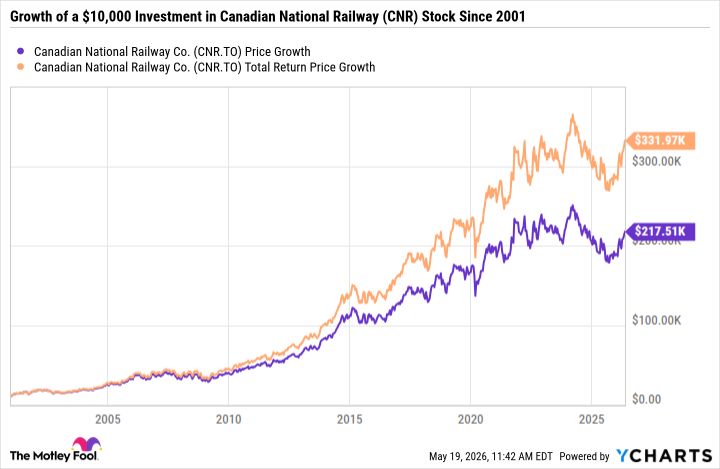

A $10,000 investment in CNR stock over the past 25 years, with dividend reinvestment, would have grown to more than $330,000 today. That’s compounding horsepower you can’t afford to ignore.

Pembina Pipeline accelerating EBITDA growth

Pembina Pipeline just raised its quarterly dividend by 3.5%, marking its fifth consecutive year of dividend increases. The Canadian oil and gas midstream giant has technically become a go-to dividend growth stock Canadian investors may depend on for passive income.

For over 70 years, Pembina Pipeline has been moving Western Canadian crude to key markets, an essential service that customers commit to under tight take-or-pay contracts, insulating cash flows from commodity price swings.

Pembina’s growth story is getting better. Management recently raised its adjusted earnings before interest, taxes, depreciation and amortization (Adjusted EBITDA) guidance for 2026, thanks in part to firm commodity prices boosting its marketing segment. Pembina expects to achieve a fee-based adjusted EBITDA per share compound growth rate of 5% since 2024, and a bullish outlook lifts that target to 5% to 7% annually through 2030.

As operating earnings grow, Pembina Pipeline’s current quarterly dividend, yielding 4.4% annually, looks increasingly secure and primed for further annual hikes.