Canadian telecom giant TELUS (TSX:T) stock is an outlier for Canadian investors seeking to build reliable passive-income generating portfolios. As the TELUS dividend yields 9.8% annually, Canadian dividend investors who naturally gravitate toward telecom giants wonder whether to chase the yield or walk away from a juicy offering. The bloated payout makes sense on the surface. Telcos offer essential services, operate at a massive scale, and have historically sustained high dividend yields.

But yields beyond 7% always signal significant danger and market skepticism. TELUS is defying the odds of a dividend cut. It may succeed and maintain the high-yield payout. Or it may not. A new CFO may chart a different financial path.

If you’re looking to build a truly diversified income stream that actually builds wealth over time, tying too much capital to a lagging telecom could be a costly mistake. Instead, look toward an under-the-radar real estate play that is quietly beating the big names at the dividend growth game: CT Real Estate Investment Trust (TSX:CRT.UN). Here’s why the retail REIT’s 5.3% yield could be a superior investment for passive income lovers.

Source: Getty Images

The TELUS trap: Capital losses a drag on portfolio returns

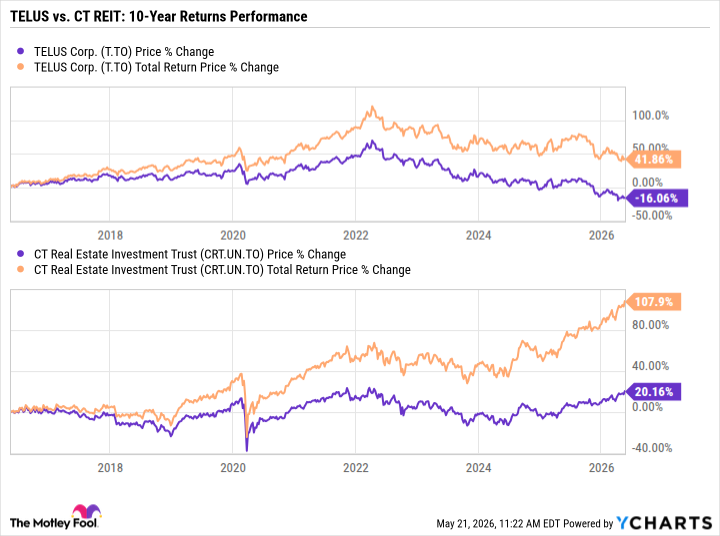

While TELUS remains a popular yield play, a look under the hood reveals a painful reality for long-term investors: its stock price has been a massive drag on overall portfolio performance. Over the past decade, TELUS delivered a lackluster total return of just 42%.

Compare that to CT REIT, which handed investors a whopping 108% total return over the exact same 10-year period. TELUS stock’s total returns lagged CT REIT’s by a wide margin.

TELUS’s headwinds aren’t over yet. TELUS management has set ambitious targets to grow free cash flow by 10% per annum, but execution risks remain as price competition subsists industry wide. With a new CFO at the helm, the pressure is on. If cash flow growth and legacy asset sales don’t materialize, the easiest route for the new financial strategist to protect the balance sheet might simply be to cut the dividend payout.

A dividend cut usually punishes the stock price, and for income lovers, a pay cut is a direct cash flow hit.

CT REIT: A safer, growing 5.3% distribution yield

To protect and diversify your income stream, you need to add cash flows backed by hard assets and unshakeable tenants to your portfolio. CT REIT’s growing portfolio of net-lease retail properties has maintained full occupancy for decades, and an average lease term of seven years going into the second quarter means the retail REIT’s rentals are secure for nearly a decade.

CT REIT pays monthly income distributions that currently yield an attractive 5.3% annually. Even better? Unlike TELUS’s frozen payout growth and a shaky dividend outlook, CT REIT is actively raising its monthly payouts. Management recently approved a 3.5% distribution increase, bumping the monthly payout to $0.0818 per unit starting July 2026. CT REIT is a dividend growth stock that has raised payouts for 14 consecutive years, providing bulletproof monthly coverage

What makes CT REIT a worthy alternative to TELUS stock for income lovers is its combination of structural distribution safety and payout frequency.

CRT.UN currently offers one of the most well-covered monthly distributions in the entire Canadian REIT space. The trust enjoys industry-leading occupancy rates at an incredible 99.4% occupancy rate. It’s dominant tenant, Canadian Tire Corporation (TSX:CTC.A), occupies 92.1% of its portfolio’s gross leasable area. Your income is practically guaranteed by one of Canada’s most resilient retail corporate backings.

Most noteworthy, in the REIT asset class, an Adjusted Funds From Operations (AFFO) payout ratio below 80% is considered excellent. CT REIT’s first quarter AFFO payout ratio sits at a highly conservative 72.5%. This gives the trust a massive margin of safety to protect, and continue growing, its distribution.

Then there’s the monthly compounding advantage. Unlike TELUS, which pays quarterly, CT REIT distributes cash 12 times a year. For investors looking to compound their wealth or cover monthly living expenses, this monthly frequency makes cash flow planning much easier.

Investor takeaway

Beyond TELUS stock’s 9.8% yield, CT REIT offers diversification through a stable, well-covered monthly payout that, combined with the REIT’s propensity for capital gains, may equal or exceed the total returns on the telecommunications giant over time – minus the anxiety of a potential dividend cut.