When evaluating Enbridge (TSX:ENB) stock as a potential long-term investment, some investors still picture a slow-moving pipelines giant built solely for defensive passive income. But if you’ve been ignoring this energy infrastructure titan lately, you’ve missed out on an absolute blockbuster run. Over the past three years, Enbridge stock has been an incredible performer.

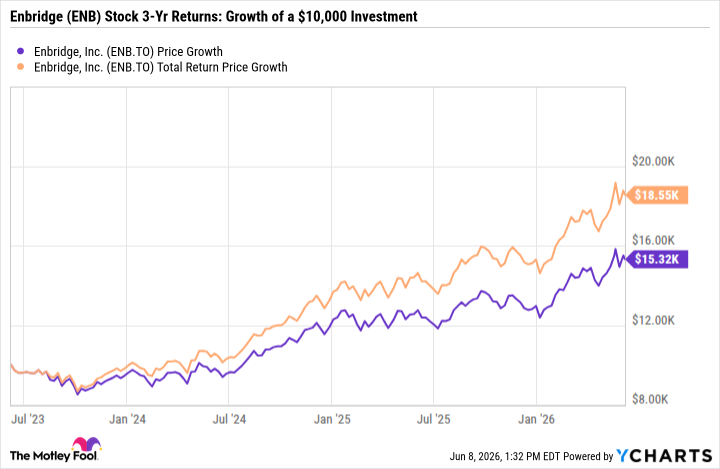

Investors who bought shares three years ago and simply held on have earned a staggering 22.8% compound annual return, translating into an 85.4% total return. That means a modest $10,000 investment, with dividend reinvestment, potentially blossomed into more than $18,500!

Of course, past performance is never a guarantee of future returns. Because the stock surged 53% over the last three years, its iconic dividend yield has shrunk from north of 6% down to 4.9% for new investors buying ENB stock today. Yet management continues its relentless, three-decade sustained efforts to raise the dividend every single year.

So, what can investors expect from ENB going forward through 2029? Let’s break down the core investment returns drivers on this re-engineered monster.

Source: Getty Images

Enbridge stock: An AI data centre backdoor investment play

Pause on chasing overhyped tech stocks at sky-high valuations for a while. Enbridge stock is quietly positioning itself as a premier backdoor play on the artificial intelligence (AI) and data centre construction boom.

The company is no longer just a liquids pipeline operation. In fact, more than 50% of its revenue could soon flow from gas transmission, gas distribution, and a rapidly expanding portfolio of renewable power projects. Tech giants require massive, unyielding amounts of power to run their next-generation data centres, and they are turning to Enbridge to secure it.

Consider the momentum building over the next three years within Enbridge’s capital investment program.

Tech behemoth Meta Platforms has signed on as a massive client, with three Enbridge power-generation plants coming online in 2027 specifically to serve Meta’s data centres. Enbridge is also executing a renewable power project to serve another major tech giant, and behemoths Toyota and AT&T. In total, Enbridge will bring into service six renewable power projects between 2026 and 2027. As a result, cash flows from these renewable ventures will grow rapidly over the next three years.

A fully re-engineered utility monster

Beyond the tech-related growth angles, Enbridge has transformed into a defensive powerhouse through its massive growth in the U.S. natural gas utility business. Management currently expects an impressive 8% compound annual growth rate (CAGR) in its U.S. utility rate base across North Carolina, Utah, and Ohio through 2029.

To sustain this growth, Enbridge’s disciplined financial engineering engages a robust, predominantly equity-funded growth model, actively executing a massive $40 billion secured capital backlog across its liquids, natural gas, and renewable power franchises.

Even better for investors concerned about dilutive share issuances: the company is committing between $10 billion and $11 billion of internally generated funds toward its annual investment capacity. This massive self-funding engine heavily reduces reliance on volatile debt markets or dilutive equity raises, keeping the company’s balance sheet incredibly strong and of high-quality.

Can ENB stock generate double-digit returns through 2029?

The investment returns potential on Enbridge stock remains exciting over the next three years. While executing on growth projects, management expects adjusted operating earnings, distributable cash flow per share (DCF/Share), and earnings per share (EPS) to grow at a reasonable 5% CAGR.

When you combine that highly visible 5% growth engine with a rock-solid current dividend yield of 4.9%, the path to wealth generation becomes incredibly clear. The dividend itself is well covered, supported by a safe DCF payout rate of 60% to 70%, with a potential dividend growth rate of 3% to 5% moving forward.

What about capital gains? Assuming valuation multiples remain constant, the stock price may track earnings and cash flow growth rates. If market sentiment doesn’t materially shift during the investment time horizon, ENB stock may potentially offer a beautiful 10% or near double-digit annual total returns over the next three years.