Understanding the 4% rule is crucial for Canadian retirees looking to manage their investment withdrawals sustainably.

Essentially, this rule suggests that you can withdraw 4% of your retirement portfolio annually, adjusting for inflation each year, without running out of money over a 30-year retirement. This strategy hinges on a balance between income generation and capital preservation.

For retirees seeking suitable dividend ETFs, it’s vital to select ones that not only yield sufficiently to meet or exceed this 4% annually but also demonstrate potential for dividend growth and capital appreciation.

Such ETFs should offer a buffer against inflation and ensure that even without reinvesting dividends, the fund’s value appreciates over time.

In Canada, only a handful of dividend ETFs have historically met these criteria. Here are the two top performers that retirees should consider for reliable, inflation-adjusted income.

Image source: Getty Images

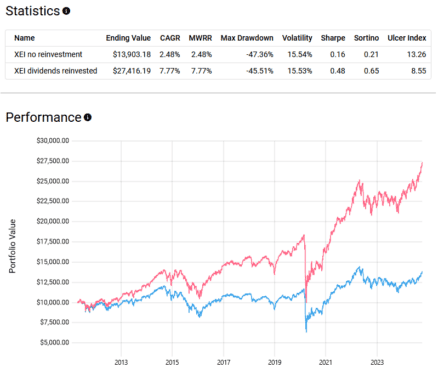

iShares S&P/TSX Composite High Dividend Index ETF

First on our list is iShares S&P/TSX Composite High Dividend Index ETF (TSX:XEI), which captures the performance of 75 stocks selected specifically for their higher yield within the broader TSX Index.

Currently, XEI offers a trailing 12-month yield of 5%, as of October 8th, with a low expense ratio of 0.22%, making it a cost-effective choice for income-focused investors. The fund also provides the convenience of monthly distributions.

Historically speaking, even if you were to withdraw and live off the dividends from XEI, your investment would still have compounded annually at 2.5%. With dividends reinvested, the return jumps to 7.8%.

Over the past five years, the annualized dividend growth rate for XEI has been 5.6%, effectively outpacing inflation and making it a robust option for retirees seeking sustainable income.

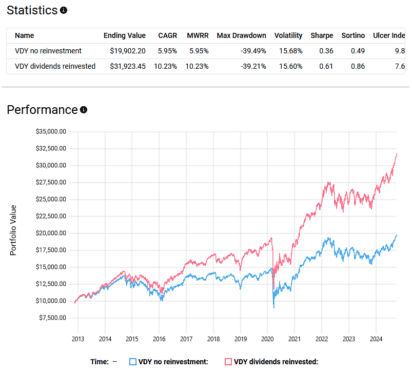

Vanguard FTSE Canadian High Dividend Yield Index ETF

An alternative to XEI worth considering is Vanguard FTSE Canadian High Dividend Yield Index ETF (TSX:VDY).

VDY is quite similar in many respects, offering a yield of 4.4%, an expense ratio of 0.22%, and monthly payments. However, historically, VDY has outperformed XEI, primarily due to its overweight position in banks, which have performed well over the past decade.

Without reinvesting dividends, the shares of VDY have historically compounded at an annual rate of 6%. With dividends reinvested, the total return jumps to 10.2%.

Additionally, the companies within VDY have increased their dividends at a faster rate than those in XEI, with dividends growing at an annualized rate of 8% over the last five years.