There’s a disturbing trend I’m seeing more and more on financial social media.

A growing number of Gen Z investors, convinced they’re permanently priced out of homeownership, are swinging for the fences with whatever capital they have. And it’s not just sports betting, prediction markets, or cryptocurrency anymore.

Now it’s exchange-traded funds (ETFs) – more specifically, ultra-high-yield, single-stock ETFs advertising double- or even triple-digit payouts. Yields of 50% or even 100% are being marketed as the shortcut to financial freedom.

But there is no free lunch in markets. If something is paying that much income a year, that money is coming from somewhere. And in many cases, chasing those yields can actually destroy more wealth than it creates.

Let’s walk through a real-world example to show you exactly why the total return math doesn’t work.

Source: Getty Images

Looking at the worst offender

Most investors are familiar with Strategy Inc. (NASDAQ:MSTR).

Originally a software company, it has effectively become a leveraged Bitcoin treasury vehicle. It issues debt and preferred shares to buy more Bitcoin. Rinse and repeat that cycle.

We can debate the sustainability of that model another time. The issue here is something else: there are now ETFs built around MSTR that advertise ultra-high yields.

A prominent example is the YieldMax MSTR Option Income Strategy ETF (NYSEMKT:MSTY).

MSTY doesn’t simply hold shares of MSTR. Instead, it holds Treasury bills as collateral and runs a complex options strategy using calls and puts designed to approximate exposure to MSTR while generating large option premiums. The upside is heavily capped.

At the time of writing, MSTY advertises a jaw-dropping 64.5% distribution yield. That number is calculated by taking the most recent weekly distribution, annualizing it, and dividing it by the ETF’s net asset value.

If you’re new to investing, that number is intoxicating. Invest $100,000, collect $64,500 a year. Financial freedom unlocked, right?

The illusion of high yield

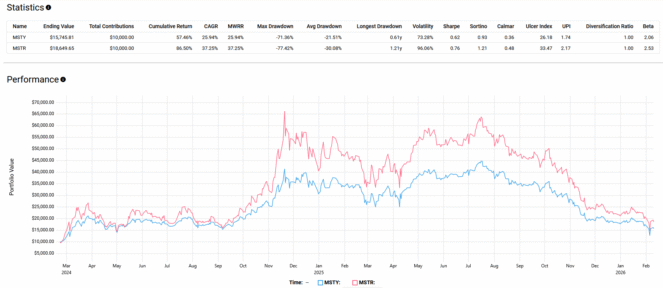

Let’s look at the period from February 22, 2024, to February 10, 2026. If you bought MSTY and reinvested every single distribution, assuming no taxes and perfect execution, you would have earned a cumulative return of 57.5%. That sounds solid.

But if you simply held MSTR stock over the same period, your cumulative return would have been 86.5%. In other words, you paid a 0.99% expense ratio for the privilege of receiving massive “income” distributions that still left you worse off than owning the stock outright.

And it gets worse. 98.6% of MSTY’s distribution is classified as return of capital. It’s your own money being handed back to you. Return of capital lowers your cost basis and isn’t immediately taxable, but economically, you’re just getting your principal returned.

So what are you really doing? You’re paying a high annual fee to receive your own money back in the form of an eye-catching “yield,” potentially triggering taxes on each distribution and underperforming the underlying stock even if you reinvest everything.

That’s financial engineering dressed up as passive income. The only person here making money is the ETF issuer. Case closed.