In a well-diversified portfolio, Canadian bank stocks have a clear and defined place. They are valuable for their reliable dividends, long-term growth, shareholder value creation, and defensive, well diversified earnings.

Canadian banks have had another great year. The two largest Canadian banks, Toronto-Dominion Bank (TSX:TD) and Royal Bank of Canada (TSX:RY) are both deserving of a spot in investor portfolios, but which of these dividend stocks looks better right now?

man withdraws money from ATM

TD Bank

TD Bank stock has benefited from very a favourable macro environment. Despite the costs and hits to its reputation resulting from the bank’s money laundering scandal, TD Bank stock has continued to rise. Since the end of 2024, TD Bank’s shares have risen more than 110%.

Strong momentum in all of TD’s businesses drove these results. In fact, TD Bank stock has enjoyed strong earnings once again in the last quarter. Adjusted earnings per share (EPS) increased 21% to $2.38 and the bank’s return on equity (ROE) increased more then 200 basis points to 14.4%. This was driven by record earnings in the bank’s insurance business, momentum in market-driven businesses, strong volumes, and margin expansion.

According to the bank’s CEO, TD Bank is looking forward to continued strong momentum and unparalleled opportunity to take market share. The bank recently increased its annual dividend by 4% and is now paying an annual dividend per share of $4.48, for a dividend yield of 2.8%.

Royal Bank

Royal Bank stock has also had a stellar year and a half, with a 60% return since December 2024, and a growing dividend.

In the bank’s second quarter results, adjusted EPS increased 27% to $3.85 and its ROE increased 270 basis points to 17.4%. These results were driven by strength in global markets and corporate and investment banking – market-driven businesses.

Furthermore, results for both TD Bank and Royal Bank also benefitted from a decline in provisions for credit losses, or PCLs, as the threat of tariffs has subsided. PCLs were markedly higher last year as the threat of tariffs was looming and threatened to negatively affect the economy.

All of this contributed to Royal Bank’s strong quarter. The bank raised its quarterly dividend by 7% to $1.76 per share and the annual dividend is currently $3.28, for a dividend yield of 2.5%.

For dividend investors, Royal Bank stock is a solid pick for 2026 as momentum is expected to continue.

The bottom line

The choice between TD Bank stock and Royal Bank stock is not an easy one. Both have well-diversified businesses, with strong capitalization and risk management practices. But in order to decide which is better for 2026, let’s review their ROEs, valuations, and dividend yields.

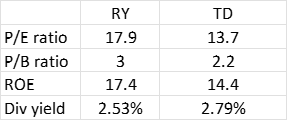

As you can see from the table above, TD Bank stock has a lower valuation along with a lower return on equity. This is partly due to the hit that resulted from the anti-money laundering scandal. But it’s also due to the fact that TD Bank stock is considered to be higher risk due to its large presence in U.S. retail and corporate banking. By contrast, Royal Bank is more heavily-weighted toward Canadian banking and wealth management, which is more stable and predictable, thus supplying more stable returns.

I favour TD Bank stock today due to its discounted valuation.